After the war-related sell-off in March, global stock markets have recovered some ground, with company earnings remaining robust and hopes of a ceasefire deal between the US and Iran beginning to rise.

A growing disconnect between fundamentals and share prices

As discussed in recent views, UK-listed quality shares have been very out of favour over the past two years, with UK market returns concentrated in asset-intensive cyclicals - most notably banks, miners and oil companies. Many financial and resources companies have trebled, quadrupled or more since 2020. They were a big part of the UK market then, and they have subsequently become an even bigger part – Financials, Basic Materials and Energy now make up nearly 50% of the FTSE All-Share. Meanwhile, the US market (and the global market by proxy) has become concentrated in and dominated by the AI capital investment trade. Trends are very polarised, with the momentum factor having its strongest run in global markets since the 1999/2000 period.

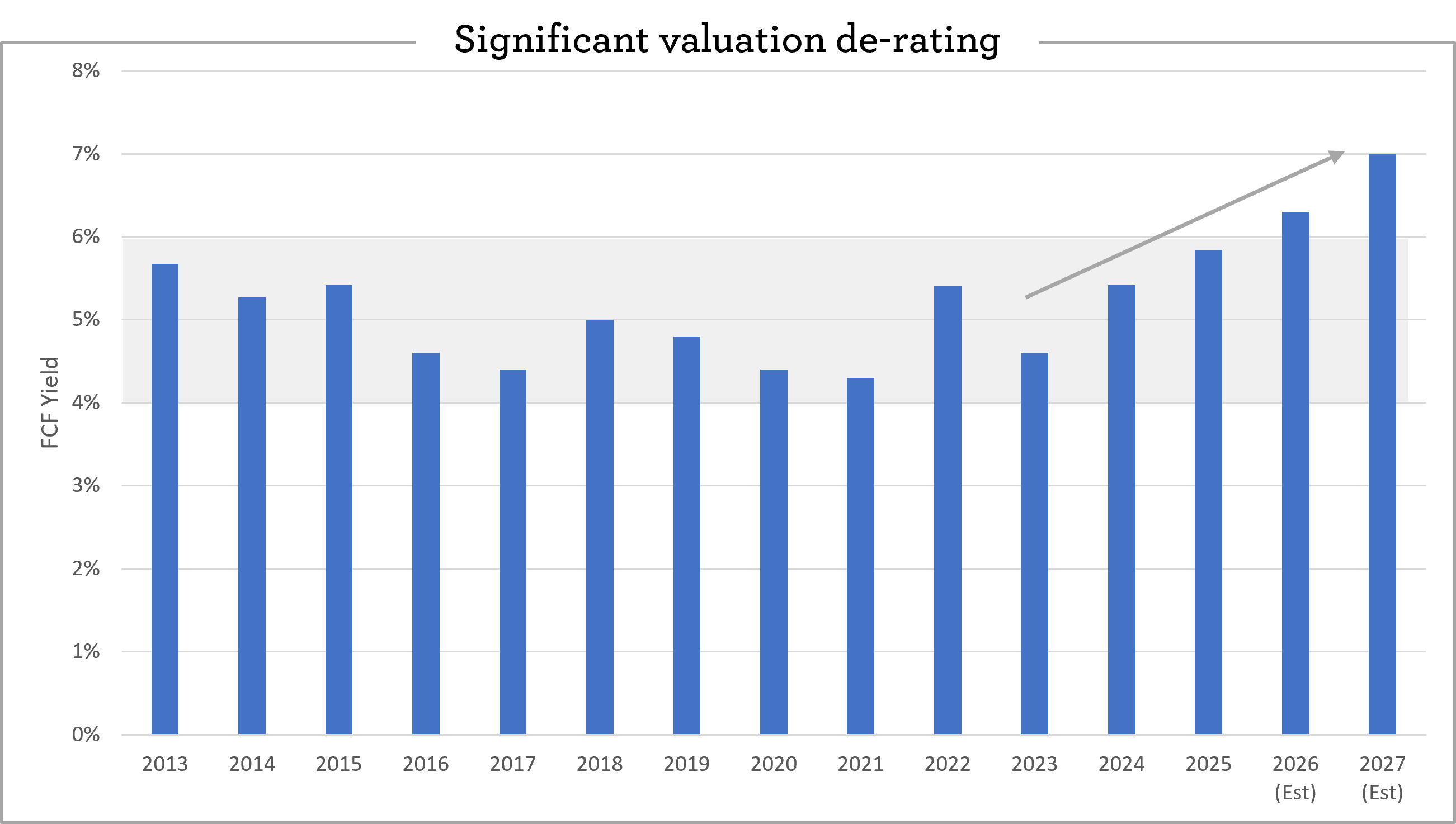

Evenlode Income’s underlying holdings continue to generate a very healthy amount of cash and – as discussed in the section below – are growing at a good rate in aggregate. Valuations have been grinding lower though. This combination of solid fundamentals and valuation de-rating has left the portfolio at its most compelling valuation since the fund’s launch in the 2009-11 period. The following chart shows the fund’s recent valuation de-rating in terms of the rise in free cash flow yieldi - a key valuation measure for us. Despite the competitive advantages, growth potential and capital-light, cash generative economics these companies enjoy, the free cash flow yield of the fund is currently higher than the FTSE All-Share Index and nearly twice as high as the MSCI World Index.

Source: Evenlode

First quarter results

The global economy has faced a challenging first five months of the year. The US economy is being helped by the staggering large investments being made in AI datacentres, but much of the rest of the global economy has faced headwinds with the Iran war triggering a spike in oil prices. Global consumer confidence - not least in the US - remains depressed.

With this backcloth, it is reassuring that the forecast for aggregate portfolio growth in 2026 remains similar to the start of the year. The expectation is for more than +5% organic revenue growthii, more than +8% organic operating profit growthiii, and double-digit earnings per shareiv growth.

Of the 35 holdings in the fund, 33 are forecast to deliver profit growth for 2026. The other two holdings, Diageo and Bunzl, are expected to deliver stable profit year-on-year.

Results round-up

With the first quarter results season now finished, below is some colour on how a range of business models held in the portfolio are faring, including a selection of this year’s faster, medium and slower growing holdingsv.

Compass (Dividend Yieldvi 2.3%; Free Cash Flow Yield 3.8%)

As the global market leader in food catering, Compass remains well placed to benefit from the structural outsourcing trend in its key end markets – Sports & Leisure, Business & Industry, Healthcare & Senior Living, Education, Healthcare and Defence, Offshore & Remote. Clients want to focus on the day job in a world of food inflation, supply chain complexity, tariffs, changing consumer dietary preferences and increased health and safety requirements. Compass has the expertise and procurement scale to manage these complexities and deliver high-quality, good-value food in a wide variety of settings.

At the latest interim results, the company reported organic revenue growth of +9% and operating profit growth of +12%, with client retention rates remaining very high at 96%. As with many management teams we speak to, the use of technology and data at scale is helping Compass grow in an efficient manner.

Spirax Group (Dividend Yield 2.6%; Free Cash Flow Yield 3.8%)

Spirax is a global thermal energy management and fluid technology solutions group. Though its industrial clients have faced higher energy costs from the Iran war, Spirax has seen a solid start to the year and maintained guidance of mid-single-digit organic growth alongside margin expansion. Spirax is very well placed to help its customers electrify their industrial processes and increase efficiency – a helpful long-term demand underpin. Much of the company’s revenue is predictably steady, generated either from maintenance expenditure, or relatively low-cost items funded from in-year operating budgets that generate an attractive, short-payback return-on-investment.

More generally, across the fund’s speciality engineering exposure, we continue to see an attractive combination of strong competitive positions, structural growth potential and valuation appeal.

Intercontinental Hotels Group (Dividend Yield 1.3%; Free Cash Flow Yield 3.6%)

IHG has also faced headwinds from the Iran war, via disruption to travel in the Middle East. Despite this, the company beat expectations for the first quarter, with +4.4% organic revenue growth, and reiterated full-year guidance:

The impact of the Middle East conflict and some wider disruption to international travel flows is expected to be more than offset by increases in demand elsewhere. Our business model is strategically diversified and resilient in capturing demand across geographies, chain scales and the different stay occasions of business, leisure and groups travel, as well as being heavily weighted to domestic and intra-regional travel.

IHG’s growth algorithm remains the delivery of +12-15% annual earnings growth over the medium-term, with very high cash conversion thanks to its franchise model.

Integrafin (Dividend Yield 3.9%; Free Cash Flow Yield 5.8%)

Integrafin has built a strong niche leadership position, via the provision of its Transact investment platform to the UK financial adviser community. Its bespoke platform, reinvestment in product development and close relationship with clients all lead to very high retention rates. Integrafin’s share of the UK adviser platform market is over 10% and steadily growing, with the company’s share of net inflows into the sector running at well over 20% thanks to its strong offering (which includes no margin being taken on interest on any client cash held on the platform, unlike many of its peers whose profitability has become dependent on this factor).

At recent interim results revenue rose +11% and earnings +14%. Management are beginning to see significant operating efficiency flow through from the investments they have made in automation and AI enhancements.

Smith & Nephew (Dividend Yield 2.6%; Free Cash Flow Yield 6.1%)

Smith & Nephew management has put some serious work over the last few years into improving the company’s operational resilience and efficiency, and its innovation function. These efforts are beginning to bear fruit, and after good growth last year the company reiterated guidance for the year of +6% organic revenue growth and profit growth at a higher rate. We think the forward Price-to-Earnings (PE) ratiovii of 12x in no way reflects the quality of Smith & Nephew’s positions in Advanced Wound Management, Sports Medicine and Orthopaedics. If the market fails to recognise intrinsic value, strategic portfolio options are possible to help unlock it.

RELX (Dividend Yield 3%; Free Cash Flow Yield 5.5%)

The digital business models held represent just over 20% of the portfolio and have been the most negative contributors to return since the start of the year. They're all slightly different, but we continue to see the competitive positions of the companies held as robust in the world of generative AI. Important factors include a combination of constantly updated proprietary data and content (that just can’t be replicated from public sources) and an overlay of continuously improving algorithms on top of these datasets. This is augmented with the specialist domain expertise they have (often in highly regulated markets where trust is key and the cost of failure is high) and deep embeddedness within customer's workflows. The consistent reinvestment they're making in product development and functionality - including generative AI – is also important. We're monitoring very closely competitor and start up activity, and we're reassured with how these holdings continue to be positioned in their markets. A discussion of RELX’s Risk division is included as an appendix to this piece, as a case study of some of the points made above.

At RELX’s latest trading update, management re-iterated full-year guidance and reported a strong start to the year, noting positive momentum across the group. Management continues to see the company as a net beneficiary of generative AI.

Experian (Dividend Yield 2.3%; Free Cash Flow Yield 6.0%)

Experian is another digital business model that views generative AI as an incremental benefit for the business. Though macro-economic conditions have been tough in its credit-related end markets, for its full-year to March 2026 Experian grew organic revenue +8% and earnings per share +13%. Earnings per share growth is also expected to be comfortably double-digit for the current year. Experian has stepped up its share repurchase programme to take advantage of the currently depressed valuation – announcing another $1bn buy-back on top of the $1bn announced in January. This means the company is in the process of buying back nearly 6.5% of the shares in issue this year.

The below quote from management is instructive from the perspective of generative AI:

Artificial Intelligence (AI) is becoming a core driver of how we operate and grow. We are embedding it across products, platforms and workflows to improve performance. It is already driving measurable efficiency gains, with a c.10-15% uplift in coding productivity in our financial year to March 2026 and select areas achieving gains of over 30%. To put this into context, labour costs, at 32% of revenue, are over 3% lower than two years ago. It is also helping us to extend our reach in existing and new markets. We have already identified over $15bn of AI-enabled addressable market opportunities, in Health, agentic commerce, Ascend platform expansion and embedded consumer marketplaces, and we are positioning the business to penetrate these emerging areas. We see accelerating internal and external opportunities as usage scales across the organisation, which will support continued margin delivery in line with our Medium-Term Framework expectations, alongside additional revenue expansion.

Unilever (Dividend Yield 4%; Free Cash Flow Yield 6.1%)

We discussed Unilever in more detail in last month’s investment view. Since then, the company released a first quarter trading statement, posting volume-led +3.8% organic revenue growth, and reiterating guidance for the year of +4-5% organic revenue growth with modest operating margin expansion.

Management noted the degree to which they have become accustomed to managing the ‘new normal’ of supply chain complexity and spikes in input cost inflation. Their reiteration of 2026 guidance includes an assumption of oil prices hovering around $115 per barrel for the rest of the year.

There is an interesting, more general point here. The last five years have included the convulsions of Covid, the Ukraine war, US tariffs and now the Iranian war. In coping with these multiple shocks, companies have become leaner machines as a result and better equipped at coping with supply shocks. Technology and data at scale have been helpful contributory tools in these efforts.

Unilever is a well-invested, growing business that has done a good job over the last decade at pivoting towards the Beauty, Personal Care, Wellbeing and Home Care categories. A forward PE multiple of approximately 14.5x (or 12.5x if one strips out the Hindustan Unilever stake) is very modest for the quality of its brand portfolio, global scale and embedded distribution network.

Howden Joinery (Dividend Yield 2.9%; Free Cash Flow Yield 5.9%)

We also discussed Howden in last month’s investment view. The company has since released a trading update. Howden reported sales growth of +3.7% over the latest period and management reiterated guidance for the current year. Howden’s in-stock model – including vertically integrated manufacturing and a near-sourcing approach – is particularly strong versus competition in times of input cost inflation and supply chain challenge.

We continue to see the company as a coiled spring. Kitchen volumes are running more than 20% below the long-term average, lower than the 2009 trough. Howden remains well invested and in a unique position to capture volume upside when it finally materialises. Though not a central expectation for us, there is a credible route to a doubling of earnings if market volumes did mean revert over the medium-term.

Diageo (Dividend Yield 2.5%; Free Cash Flow Yield 6.2%)

At the recent third quarter trading statement, Diageo management reiterated guidance for flat to low-single-digit profit growth in the current financial year. Strong growth from Guinness, Latin America and Africa was offset by continued weakness in US Spirits. We view the downturn in the US spirits category as a combination of affordability and health-related trends, but with affordability being the more significant factor. New management are investing behind Guinness to drive continued growth, whilst also taking steps to meet the pressured US consumer where they are with mid-tier price points and ready-to-drink products both areas of focus. Recent discussions with management suggest that the potential for improving profitability over time is also significant. Diageo’s forward PE multiple is 13x – very depressed, in our view, for an excellent portfolio of global brands.

Bunzl (3.3% Dividend Yield; Free Cash Flow Yield 8.6%)

Bunzl and Diageo are expected to deliver the least progress in operating profit this year, with a flattish result forecast for both. Bunzl had a tough year last year with a strategic misstep in its North American division. The company’s recent trading statement was reassuring, reconfirming guidance for the year and the continued improvement in last year’s problem division. Bunzl also noted that the acquisition pipeline remains healthy. These bolt-on acquisitions are a key part of the long-term growth model, given the highly attractive returns-on-capital that the company can generate from them.

Bunzl is another holding – on a forward PE of 12.5x – that is being given little or no credit for the quality of its compounding model (+9% earnings growth per annum over 20 years), its high returns on capital, and its prodigious cash generation.

The fundamental algorithm

Markets have become increasingly driven by narrative and momentum over recent months, but the long-term laws of investment haven’t been repealed. The total return algorithm for the fund suggests a strong fundamental return from here. A 3% dividend yield and a 2% buyback yield mean that earnings growth of 5% or more is all that’s needed to drive a total return of more than 10%, assuming no change in valuation.

If anything, recent announcements suggest the buy-back yield is heading up above 2% on a forward-looking basis, with 80% of holdings now actively buying shares.

The problem for total returns over the last two years has been that the portfolio has been getting steadily cheaper. This de-rating trend only needs to stop to allow the total return algorithm to shine through. Given how depressed current valuations are relative to history and to global peers, we also see the potential for a significant valuation re-rating of the portfolio over time, this would be the icing on the cake.

Hugh, Chris M., Ben P., Charlotte, Leon and the Evenlode team

29 May 2026

RELX: Risk business deep dive

RELX was lobbed into the AI losers basket in May last year and has lost 40% of its market capitalisation since. This looks deeply unwarranted to us. The majority of RELX’s profit is generated from businesses with no or extremely low AI disruption risk – physical events and exhibitions, academic journals and its Risk division, the subject of this piece. The businesses where Generative AI is more applicable - mainly the Legal business - have deep data and content moats and are already applying the technology very successfully to accelerate growth.

Management have responded well, in our view. Firstly, they continue to drive strong financial results and invest heavily in technology, with organic revenue and earnings growth of +7% and +10% respectively in 2025, and similar growth expected in 2026. Secondly, the company has increased buybacks, which makes sense given the shares are trading at a highly attractive valuation, with plans to spend £2.25bn in 2026, over 5% of the current market capitalisation, and a material step-up from the £1.5bn spent in 2025. Third, management are actively engaging with investors and the market community. We met with CFO Nick Luff at their head office on the Strand last month, and this week we attended their seminar on Risk Business Services (also known as LexisNexis Risk solutions), which included a question-and-answer session with the Business Services CEO, Rick Trainor and Chief Technology Officer, Vijay Raghavan. The Risk division accounts for 40% of RELX’s profit, and Business Services is the largest business within Risk, representing 18% of group profit.

Business Services is a B2B franchise mainly focused on the risk assessment of individuals and transactions to help prevent fraud and improve transaction efficiency. To take one product example, when an individual logs into their bank account, RELX's platform provides a real-time risk assessment by cross-referencing device, location and behavioural data across its network to determine whether the person at the keyboard is who they claim to be.

The seminar further substantiated our view of the wide economic moat around the Risk business. It owns vast data assets that create several layers of competitive advantage. First, the business has assimilated tens of billions of public records, from tens of thousands of sources, over multiple decades. Some of the data is no longer publicly available, and some is theoretically public but extremely difficult and complicated to collect because of the format, or because it requires manual collection. Second, the division owns 25 continuously updated proprietary contributory databases. These are not publicly available and would be effectively impossible to fully replicate, presenting a severe chicken-and-egg problem for potential new entrants. It would require decades of relationship building and enormous customer trust to build them from scratch. Importantly, these contributory databases drive a significantly higher number of the daily signals (logins, account changes, applications) in the Risk network than the public and licensed data. Then – and this is particularly key for the division’s competitive advantage - continuous feedback loops mean each additional signal created in the network (over 400 million are added every day) enriches the underlying models, compounding RELX’s predictive advantage over time, and therefore continuously raising the barrier for potential new entrants. Customer retention is very high, 97%+, with an impressive customer roster including 98% of global top 50 banks, 90%+ of US credit card issuers and 50%+ of Fortune Global 500 retailers.

Generative AI is very applicable in RELX’s Legal business, driving higher growth but also concerns in the market around disruptive new entrants, which we have written about previously. In Risk, the CTO highlighted that over 90% of transactions are machine-to-machine, where the company provides scores and attributes requiring accurate deterministic outcomes, best suited to extractive AI technologies, which RELX have been developing for more than 15 years. This is consistent with discussions we have had with technologists and industry experts. RELX are by no means dismissive of generative AI, however, which they are layering on top of the extractive AI for certain use cases such as image sorting, facial ID checks and for mapping raw unstructured data into structured data. They are also using Generative AI for coding and development purposes, with scope for significant efficiency gains over time; RELX spends $2bn annually on technology and employs more than 12,000 technologists across the group.

RELX’s Risk division is the global market leader – number one in physical and digital identity data and in financial crime screening, and management noted that whilst they do see start-ups entering the market, as they always have, these compete at the fringe, lack the data moat and infrastructure, and find it challenging to reach scale positions. Risk has grown organic revenue consistently in the +7-9% range, and demand for their products is increasing as the number and sophistication of fraud attacks grows, compounded by the rapid development of generative AI – synthetic identity attacks, for example, have tripled over the past year. While an unwelcome development for all of us, this further increases the mission-critical nature, and demand, for RELX’s risk products.

Despite RELX’s improving growth trajectory, the shares are trading at their cheapest for over a decade, trading on a PE of 16x, a dividend yield of more than 3%, and a free cash flow yield of 6%. The dividend and buyback yield total 8%, which together with forecast operating profit growth of +7%, points to a 15% total return if the current, highly depressed valuation, remains unchanged. We look forward to RELX’s next investor seminar on the Journals business later this year.

Important information

Evenlode has developed a Glossary to assist investors to better understand commonly used terms.

Market data is sourced from S&P Capital IQ, Financial Express Analytics and Bloomberg unless otherwise stated.

This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject to change and are not guaranteed.

IFSL Evenlode Income is a sub-fund of the IFSL Evenlode Investment Funds ICVC. Full details of the Evenlode Funds, including risk warnings, are published in the IFSL Evenlode Investment Funds Prospectus and the IFSL Evenlode Investment Funds Key Investor Information Documents (KIIDs) which are available on request and at www.evenlodeinvestment.com.

The IFSL Evenlode Investment Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, IFSL Evenlode Income may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

FTSE® is a trademark of the relevant London Stock Exchange Group plc (“LSE Group”) companies and is used under licence. FTSE Russell is a trading name of certain LSE Group companies. All rights in FTSE Russell indices and data vest in the relevant LSE Group company. Neither LSE Group nor its licensors accept any liability for errors or omissions in the indices or data, and no reliance should be placed on this information. Redistribution of LSE Group data is prohibited without prior written consent. LSE Group does not promote, sponsor, or endorse the content of this communication.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited (IFSL) is authorised and regulated by the Financial Conduct Authority, No. 464193.

Footnotes

-

Free Cash Flow Yield - Free Cash Flow (FCF) per share divided by the current share price. A higher Free Cash Flow Yield implies a company is generating more cash that could be paid out as dividends and to reinvest into growth of the business.

-

Organic Revenue Growth – The percentage increase of sales generated from a company’s existing resources and operations. Excludes growth attributable to mergers and acquisitions and foreign exchange.

-

Organic Operating Growth – The percentage increase of earnings derived from a company’s existing operations. Excludes growth attributable to mergers and acquisitions and foreign exchange.

-

Earnings Per Share (EPS) - A measure of company profitability, calculated by dividing a company’s profit by the number of shares in issue.

-

Source: Evenlode, Visible Alpha for all Dividend Yields and Free Cash Flow Yields. All current financial year.

-

Dividend Yield - Annual dividends made by a company to shareholders, expressed as a percentage of the share price.

-

Price-to-earnings ratio - A measure of a company’s current market valuation compared to its earning potential, calculated by dividing a company’s share price by its Earnings per share (EPS).