February was characterised by very high geopolitical uncertainty and market volatility; tensions built in the Middle East, the US Supreme Court ruled Trump’s liberation day tariffs illegal, and nerves around AI disruption risk rippled through the market sector-by-sector. IFSL Evenlode Incomei rose +4.0%, compared to a rise of +3.9% for the IA UK All Companies sector and +6.5% for the FTSE All-Share. The UK market’s strength was helped by another strong month for commodity stocks which, along with financials, have become a large part of the index over the last two years. This took the year-to-date return to +2.4% for IFSL Evenlode Income compared to +6.6% for the IA All Companies sector and +9.7% for the FTSE All-Share.

In early March, stock markets have fallen as oil prices spiked due to the closing of the Strait of Hormuz.

Is quality investing dead?

A few articles have appeared over recent weeks in the financial press, entitled ‘is quality investing dead?’ or something similar. The contrarian in me is reminded of similar articles from the late 2010s and 2020, entitled ‘is value investing dead?’. My father is a dyed-in-the-wool value investor, and I remember his pain at the time. Over the last five years, and particularly over the last eighteen months, it has been the turn of quality investors to feel the pain of relative underperformance.

Arguments against any asset class or investment approach always have a truer ring to them following a period of prolonged relative underperformance. The key argument currently deployed against quality stocks is that high-return, competitively advantaged companies are ‘long duration’ assets. In other words, their earnings and cash flows are more highly rated by investors because there is an expectation that their cash flows will continue long into the future, thanks to the strength of their franchises and their long-term growth opportunities.

The critique then goes on to suggest that these long duration companies shouldn’t be valued as highly anymore, for two main reasons:

- Interest rates are higher than they were five years ago, and therefore the opportunity cost of waiting for those longer-term earnings to come through is now higher.

- We are in a world of rapid technological change and so, in theory at least, even the best businesses are prone to disruption risk. Everything is more uncertain.

Long duration no longer

What I find striking is how far this narrative has now been taken, in terms of the extent to which it has embedded itself in relative valuations.

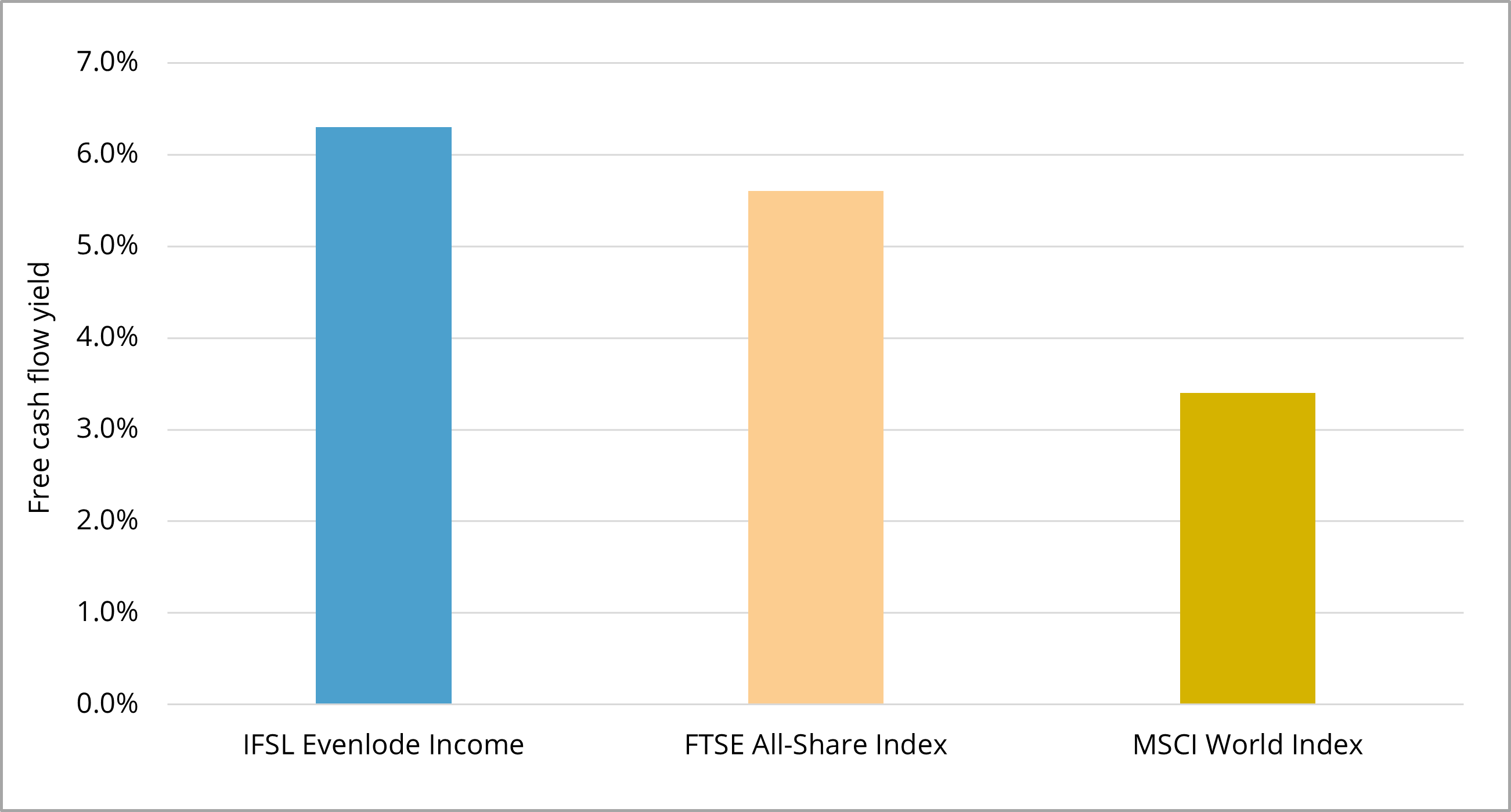

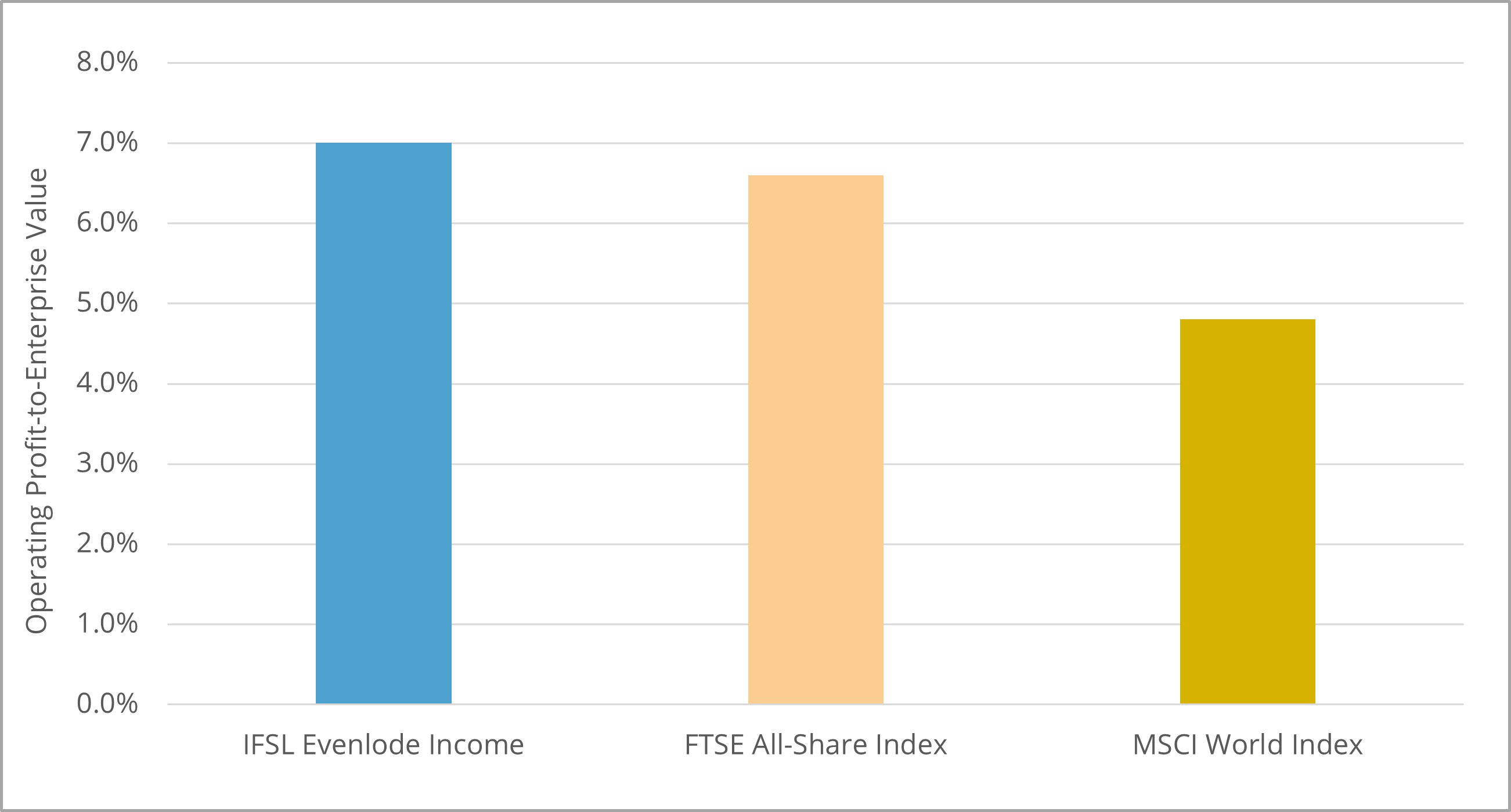

The holdings in the IFSL Evenlode Income portfolio – growing companies that possess durable competitive advantages and deliver high returns on capital – are back to valuation levels we remember from the 2009-11 period in absolute terms. They are also currently cheaper on aggregate than the UK market, and very substantially cheaper than the global stock-market. Below is IFSL Evenlode Income’s valuation on a last-twelve-month free cash flow and earnings basis – versus both the UK and the global market. In summary, these companies are being given no credit for their competitive advantages, highly cash generative characteristics and low-leverage business models.

Free cash flow yieldii

Earnings yieldiii

HALO

There is also a sentiment doing the rounds that high-return, asset-light businesses are more prone to disruption than asset-intensive businesses, in the current era. This theme is represented by the acronym HALO (heavy assets, low obsolescenceiv). Part of the argument here is that high-return, asset-light businesses are often digital in nature, and therefore may be more at risk from technological disruption. I agree with this argument up to a point, though I’m strongly of the view that the best placed digital companies can harness AI technology, remain in good health, and continue to grow at good rates. A companion argument in favour of HALO companies is that there is likely to be more investment over coming years in physical areas of the economy, such as energy security and efficiency, and national infrastructure renewal.

On this point many asset-light, high Return on Capital Employedv (ROCE) companies do own and sell plenty of assets and physical products. Pictured below are manufacturing facilities at IFSL Evenlode Income holdings Rotork, Weir Group and Howden Joinery. They are in the business of making and selling physical things, but they generate very attractive ROCEs - of +38%, 18% and 19% respectively - thanks to the strength of their competitive positions. The high ROCE is generated by a variety of factors that define their strong franchises including brand strength, product and service quality, entrenched distribution networks, R&D expertise, and the mission-critical nature of their products versus the low percentage of customer budgets they represent.

Investment in national economies will be crucial in the coming years with the goal of driving better growth and resilience. Structural trends include the need for investment in digitalisation and automation, research and development, health care, upgraded infrastructure and industrial facilities, and improved energy efficiency and security. Many portfolio companies are well placed to meet these needs.

Competitively advantaged companies are not dead

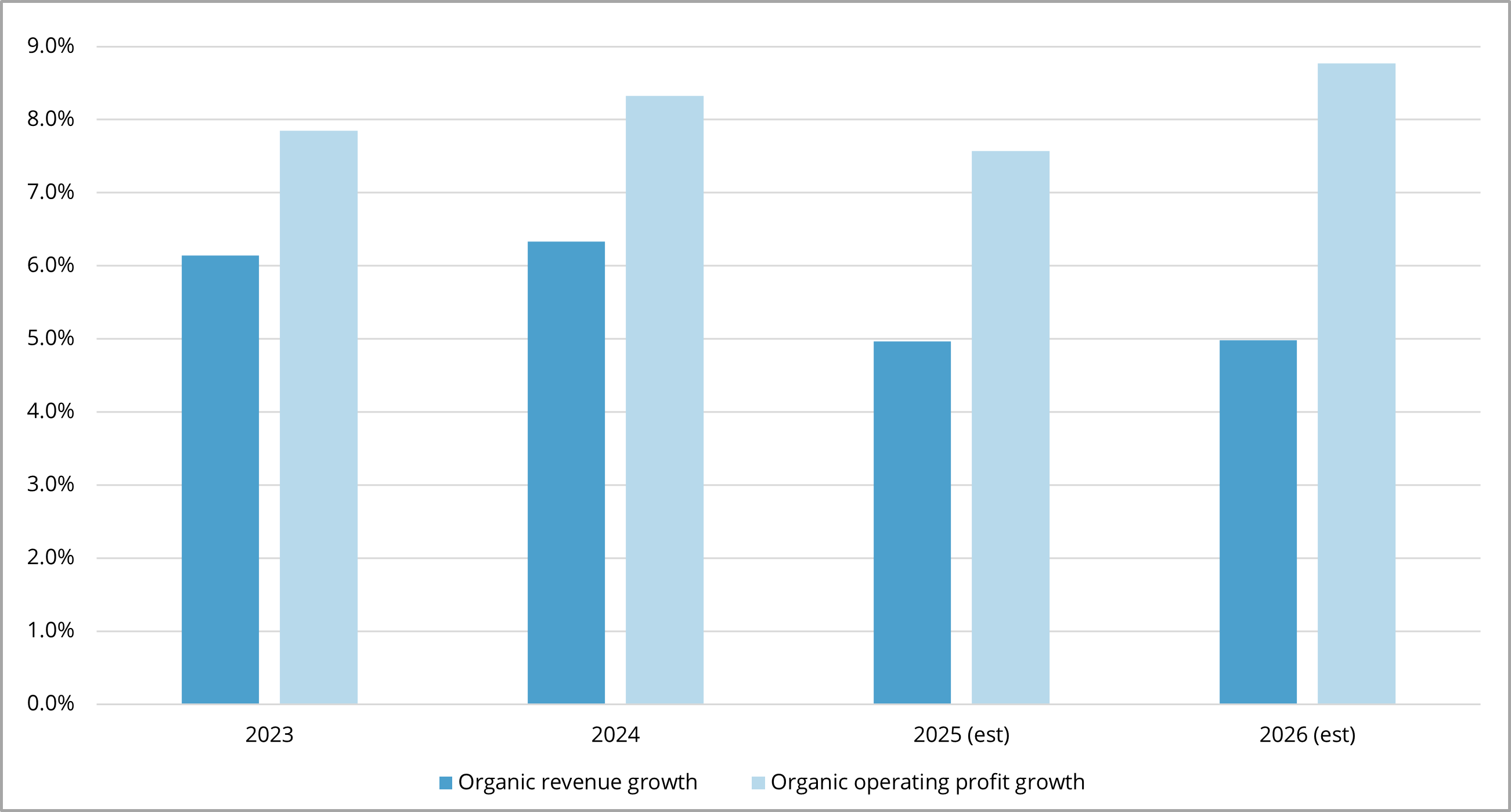

This leads back to the actual companies we invest in. Though share prices and valuations are highly depressed for many holdings, and the world is clearly not without significant complexities, the portfolio continues to grow at a good rate whilst spinning off very large amounts of free cash flow. Below is the recent organic revenuevi and profit growth for the portfolio and the current forecast for 2026, and I will discuss recent results in next month’s investment view in more detail.

2023 – 2026: Revenue and profit growth

Companies eating themselves

As discussed above, even after making significant operating and capital investments in their businesses, portfolio holdings are generating plenty of excess free cash flow, which leaves room for share buy-backs as well. Returning to the digital-orientated holdings RELX, Experian, LSEG and Sage grew organic revenue at +7%, +8%, +7% and +10% during their latest respective reporting periods, and free cash flow generation was strong. Since the start of the year, each company has announced a buy-back programme representing approximately 7%, 6%, 4% and 3% of shares in issue respectively, to be completed by the end of 2026. This significant de-equitisation is highly accretive to owner earningsvii.

As investors in UK quality companies, we are the first to acknowledge that we have been fishing in a deeply unfashionable pool of the global stock market over the last few years, but this has created a valuation opportunity that is commensurately compelling.

Hugh, Chris M., Ben P., Charlotte, Leon and the Evenlode team

16 March 2026

Evenlode has developed a Glossary to assist investors to better understand commonly used terms.

Market data is sourced from S&P Capital IQ, Visible Alpha, Financial Express Analytics and Bloomberg unless otherwise stated.

This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject to change and are not guaranteed.

IFSL Evenlode Income is a sub-fund of the IFSL Evenlode Investment Funds ICVC. Full details of the Evenlode Funds, including risk warnings, are published in the IFSL Evenlode Investment Funds Prospectus and the IFSL Evenlode Investment Funds Key Investor Information Documents (KIIDs) which are available on request and at www.evenlodeinvestment.com.

The IFSL Evenlode Investment Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, IFSL Evenlode Income may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

FTSE® is a trademark of the relevant London Stock Exchange Group plc (“LSE Group”) companies and is used under licence. FTSE Russell is a trading name of certain LSE Group companies. All rights in FTSE Russell indices and data vest in the relevant LSE Group company. Neither LSE Group nor its licensors accept any liability for errors or omissions in the indices or data, and no reliance should be placed on this information. Redistribution of LSE Group data is prohibited without prior written consent. LSE Group does not promote, sponsor, or endorse the content of this communication.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited (IFSL) is authorised and regulated by the Financial Conduct Authority, No. 464193.

Footnotes

-

B Acc shares.

-

Free cash flow (FCF) - A measure of how much cash a company can generate over and above normal operating expenses and capital expenditure. The more FCF a company has, the more it can allocate to dividend payments and growth opportunities. FCF yield - Free Cash Flow (FCF) per share divided by the current share price. A higher Free Cash Flow Yield implies a company is generating more cash that could be paid out as dividends and to reinvest into growth of the business.

The Free Cash Flow Yield for a portfolio/ index is the total free cash flow generated by a portfolio or index, divided by the market value of the companies in the portfolio or index.

-

Earnings yield is calculated as operating profit divided by enterprise value and indicates the return an investor receives on the entire business from its operating activities, before financing and tax effects. Enterprise value = Market capitalisation + net debt.

-

Examples of HALO companies would be utility companies and transport infrastructure companies.

-

Return on Capital Employed shows how much operating profit a company makes for every pound of capital it uses in its business.

-

Organic revenue excludes the impact of foreign exchange and mergers/acquisitions.

-

Share buybacks lead to fewer shares in the market, with each share representing a slightly bigger slice of the company.