The last few weeks have been very turbulent for geopolitics. The outbreak of war in the Middle East at the start of March sent shockwaves through global markets, with a ceasefire announced just after month-end. The March sell-off was broad-based across equities and bonds, with just about the only area of positive performance in markets coming from the energy sector.

Since the start of the year, IFSL Evenlode Income’s return is now -1.1% compared to +4.4% for the IA UK All Companies sector and +6.3% for the FTSE All-Sharei. The main drags on relative performance since the start of the year have been the fund’s lack of mining and oil exposure, and the exposure to digital business models (c20% of the portfolio) which sold off on AI-related worries in the first few weeks of the year.

The fund’s holdings are resilient market leaders with strong competitive positions, and we are confident their qualities will be recognised again by investors in due course. We think the current opportunity set in our investable universe is as broad as it has been since the 2009-2011 period when we launched the fund, as we discussed in last month’s investment view ‘Is Quality Investing Dead?’.

This broad-based valuation appeal was exemplified by test and inspection company Intertek’s strong trading update, strategic review, and subsequent announcement of a rejected bid approach last week. Despite rising more than +35% from its lows on this news, the stock still offers a very attractive 3.5% dividend yieldii and a 5.2% free cash flow yieldiii.

Results and valuation

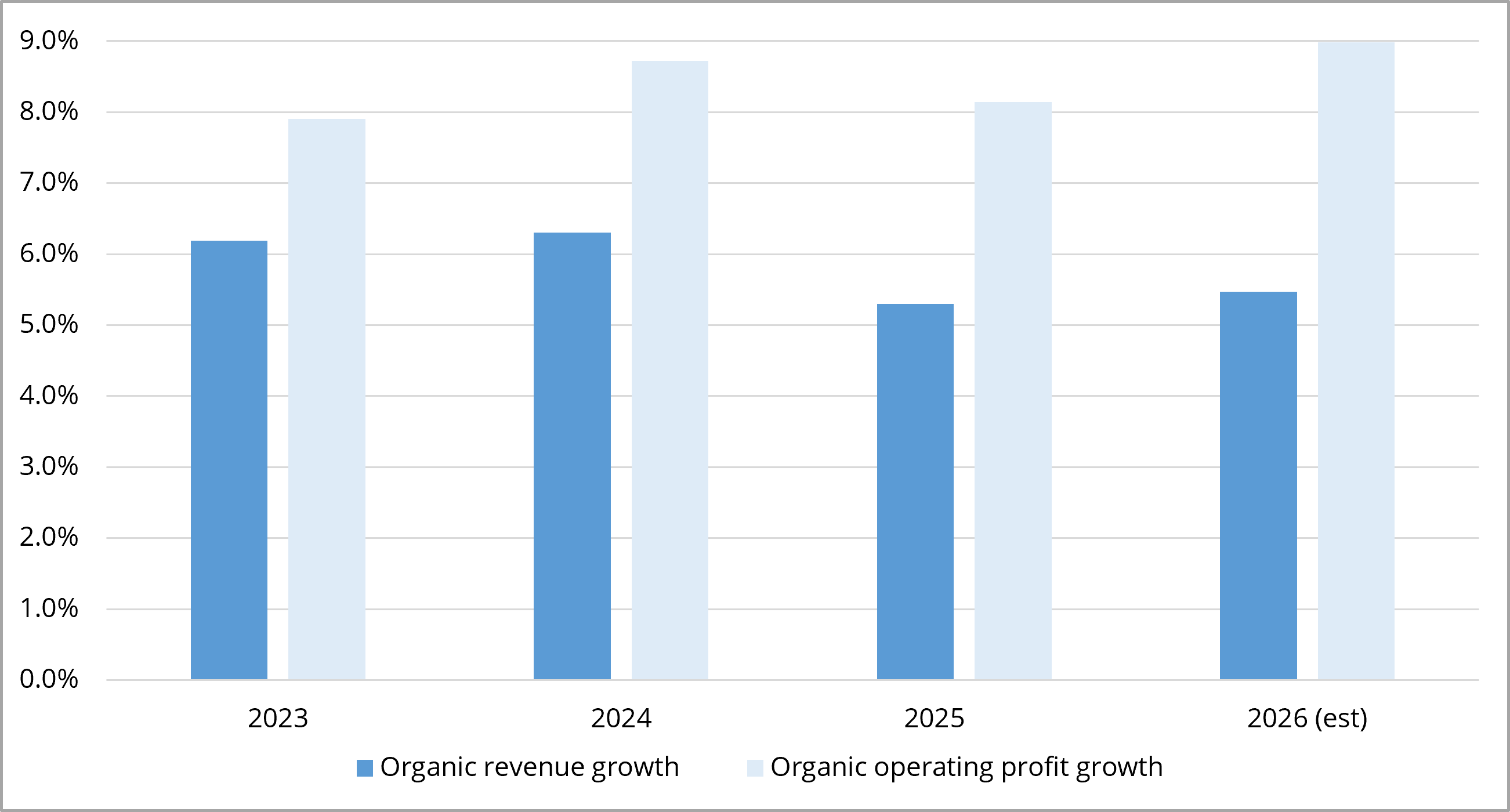

In terms of operating fundamentals, the portfolio continues to grow at a decent rate. The chart below shows growth in organic revenue and operating profit for the portfolio over recent years and the current forecast for 2026iv.

The war in the Middle East, and the commensurate rise in the oil price, is presenting input cost and supply chain challenges for many companies and is also putting further pressure on the global consumer. In this context, it is reassuring that growth expectations for 2026 are thus far effectively unchanged (in fact slightly up) since the start of the year, with +5% organic revenue growth and +9% organic operating profit currently expected. The portfolio continues to generate a huge amount of cash, and many holdings are buying back large quantities of shares at attractive prices.

This month, we will discuss several holdings that we have met with over the last month to give some flavour of what we are hearing on the ground.

Engineers

We increased exposure to several of our specialist engineering holdings in March. Their share prices fell back in the war-related March sell-off, but we see these companies as very well placed to take advantage of structural investment trends in their end markets – energy security, energy efficiency, national infrastructure renewal, defence, industrial automation, and the electrification of the industrial sector. These holdings benefit from durable competitive advantages, so they can turn demand growth into attractive and durable value creation for shareholders.

Rotork

We met with Rotork management at their headquarters in Bath following full-year results. Rotork makes and services the specialist actuators and flow control equipment that open and close valves in industrial settings – from oil refineries to water treatment plants and pharmaceutical facilities. Rotork’s global service network - which maintains and repairs equipment already installed at customer sites - is a particularly attractive part of the model. It now represents a quarter of group sales (and more than half if replacement equipment relating to these service visits is included). Once Rotork’s equipment is installed, customers almost always rely on Rotork to keep it running.

Rotork has been an outstanding long-term compounder, as the below total return chart shows:

Rotork launched its ‘Growth+’ strategic plan in 2022, and over the last three years revenue growth has averaged +8% per annum and margins have steadily ticked higher. The share price, though, has been stuck in neutral for several years now. The stock has therefore been getting steadily cheaper, both in absolute terms and relative to its peers - a consistent theme across our universe of UK-listed global market leaders. Rotork has a net cash balance sheet and has been steadily buying-back shares.

Full-year results confirmed another year of steady progress with orders up +6%, revenue +4%, and operating profit +10%. The company is benefitting from a combination of growth drivers including energy security investment, methane reduction and the transition to electric actuators - a shift driven by structural trends in automation, electrification, and digitalisation. As part of the company’s ‘Growth+’ plan, Rotork is also targeting newer and high growth markets to diversify the business, including water infrastructure, nuclear, HVAC (heating, ventilation, and air conditioning), desalination, datacentres and carbon capture.

The Iranian conflict is creating short-term disruption for Middle Eastern clients. But in Rotork’s traditional oil and gas business - which represents 45% of revenue - damaged infrastructure in Qatar and Bahrain will need repairing over the next couple of years. Gulf Cooperation Council states are already looking at projects to diversify their energy distribution infrastructure, including more pipelines to the Red Sea and the Mediterranean. Countries around the world - particularly Asian countries such as India – are also highly likely to increase investment in energy infrastructure (refining capacity, LNG facilities etc.) given the energy security vulnerabilities that recent events have brought into stark relief.

Rotork actuators have an exceptional reputation for quality and are mission-critical to the large industrial facilities into which they are installed but represent a very small proportion of overall build and running costs. This leads to an attractive business model, and the benefits include – as with many Evenlode holdings - strong pricing power, high gross margins, and therefore an ability to deal successfully with input cost inflation when needed.

Our recent conversations with the management of Smiths, Spirax and Weir also give us confidence on the long-term opportunity that they can capture within their industrial and infrastructure-exposed end markets.

RELX

As discussed in recent investment views, RELX’s share price has been caught up in the debate around the potential disruption of digital businesses through generative AI, and in particular Anthropic’s Claude Code and Claude Cowork offerings.

We met with management in London after full-year results to discuss recent operational trends and their longer-term strategic thoughts. Management continue to view RELX as a net beneficiary of generative AI, both in terms of harnessing the technology to enhance its offering to clients and also utilising AI tools to increase productivity.

RELX owns huge, irreplicable, proprietary datasets that are continuously cleaned, refreshed, updated and enhanced. The company’s competitive advantages rest not just on these datasets, but also on self-improving algorithms that are constantly trained and refined on the vast usage data that flows through RELX’s network every day. RELX also benefits from high switching costs. The company mostly services clients in heavily regulated markets where reputation is sacrosanct, long-term trusting relationships are key, and products also become deeply entrenched in workflows.

The above characteristics are not things that a start-up can recreate from scratch or simply ingest from the ‘common crawl’ (i.e. the entirety of the public internet).

RELX has been harnessing AI technology for well over 15 years and management has been busy embedding generative AI in its products where relevant over the last four years. RELX’s legal division LexisNexis - which represents 12% of group profits but has been the biggest focal point for the AI debate - is a case in point. Over the last few years, the steady adoption by law firms of legal analytics, and now the increasing adoption of generative AI functionality, has led to an acceleration of growth in this division. LexisNexis revenue grew by +9% in 2025. Management see a long runway for growth in this division, as law firms continue to adopt and deepen their usage of the LexisNexis platform’s generative and agentic AI functionality.

LSEG

London Stock Exchange Group (LSEG) has also seen considerable share price pressure over recent months due to AI disruption fears surrounding its data and analytics divisions which represent 44% of group revenue. These fears are in sharp contrast to continuing strong profit growth. Though generative AI is clearly a transformational technology, we view the risk for data analytics companies to be heavily skewed towards providers who primarily curate and distribute publicly available information, particularly if that information is relatively static. As with RELX, LSEG's core proposition does not fit that description. 98% of its data is proprietary, including exchange-sourced, real-time data distributed under tightly regulated agreements. The recent long-term (up to 7 years) data and analytics contracts signed by Citi, HSBC, UBS and BNP suggests that these clients agree. The data is so deeply embedded into their risk engines, order management systems and settlement systems that switching is not a viable option within a near-term time horizon. We are not ignoring the risks. Workspace seat attrition is a reasonable concern, especially if AI reduces the need for some bundled analytics and junior workflow users. However, this is more than offset by the opportunities available to LSEG from the new technology.

The LSEG MCP (Model Context Protocol) server - launched only weeks before recent results - already has more than 60 institutions connected with a strong pipeline behind them. Many of the connecting users are individuals at existing customer organisations with no prior LSEG data relationship, so the channel is expanding reach within the installed base and providing new sales leads at no cost.

The deeper opportunity is in how AI changes the economics of data consumption itself. LSEG's current subscription model is volume-agnostic; a bank pays a fixed fee regardless of how intensively its systems use the data. As AI agents and models are layered into financial workflows, data consumption per customer grows dramatically. Humans - as management have noted - barely scratch the surface of available data while models consume vastly more. LSEG is moving deliberately toward a hybrid subscription-plus-consumption pricing model that captures that incremental usage in revenue. As the installed base of AI agents within financial institutions grows, and as more of LSEG's data becomes accessible via MCP, the revenue opportunity expands.

Against this backdrop, the valuation is compelling. LSEG has delivered accelerating organic growth and double-digit earnings per share growth over the last two years. Despite beginning to recover from lows, the stock still offers a forward free cash flow yield of 7.3% and a forward P/Ev of 18.6x. 20% of LSEG’s valuation can be attributed to its stake in Tradeweb, which generates only 13% of group revenues. Splitting out the company’s Tradeweb stake (at market price) therefore improves valuation multiples by a further 5-10% for the remaining business. Management have also demonstrated their belief in the valuation opportunity, announcing a £3bn buyback alongside results, equivalent to 7% of the market cap. We believe that this action will be highly value enhancing for those shareholders that remain.

Howden Joinery

Howden returns us from the digital world to the world of cabinetry and work surfaces. The company sells kitchens and joinery products to local trade builders through a network of nearly 900 UK depots, supplemented by a growing presence in France and Ireland. The model is a distinctive one; autonomously run depots within very clear financial guardrails, vertically integrated manufacturing, an in-stock model, and a sophisticated logistics and digital platform. Developing trust and long-term relationships with local builders is key - many even gather at Howden depots for complimentary coffee to start the day!

Howden has been another long-term compounder over the years, though as with Rotork, the share price has struggled to make progress over the last five years, as evidenced by the total return chart below:

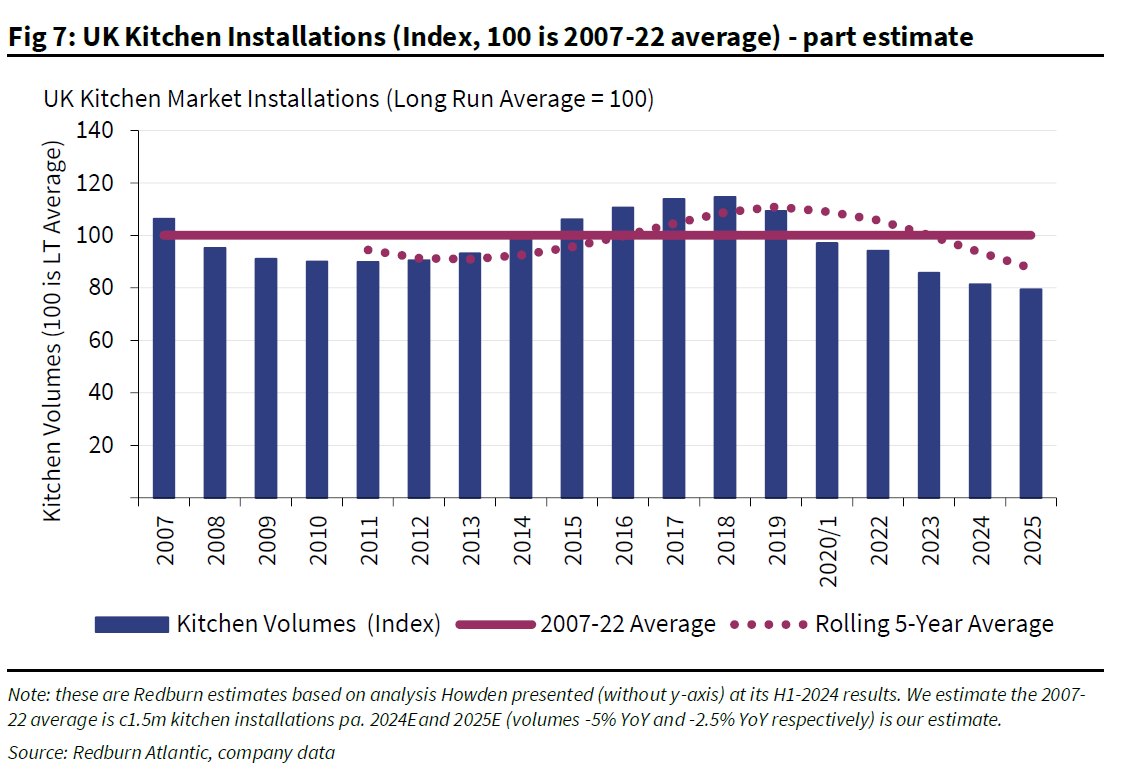

We met with CEO Andrew Livingston and CFO Jackie Callaway after their full year 2025 results, which were very solid given the backdrop. As the following chart highlights, overall kitchen volumes declined to lower levels than even 2009 last year.

The 2024 autumn statement was also a considerable headwind for Howden in 2025, due to both the employer’s national insurance and minimum wage increases.

Despite all this, Howden delivered revenue growth of +4% and earnings per share growth of +8%. The business gained share, opened 23 new depots, delivered productivity savings and utilised its strong net cash position to buy-back shares.

When we spoke in March, management acknowledged a potential dent to sentiment from the war in the Middle East and expected the UK market to be roughly flat in volume terms for the year. Whatever the final outcome, Howden is well placed to keep steadily gaining market share, helped by new product ranges, an expanding depot estate and the continued roll-out of its pricing analytics tool, which is already improving profitability. The company has a clear six-year runway of new depot openings and a pipeline of growth levers at the individual depot level including premium solid-wood kitchens, bedrooms, worktops, and accessories.

The stock offers a dividend yieldii of 2.7%, a free cash flow yieldiii of 5.6% and a net cash balance sheet which provides the firepower for ongoing share buy-backs. Howden remains extremely well-invested, and when volumes finally begin to recover, the company is in a unique position to take advantage of the upside.

Unilever

Consumer Staples stocks represent 15% of the IFSL Evenlode Income portfolio, with Unilever the largest holding. The sector has faced a tricky operating backdrop during the post-Covid cost-of-living crisis, but cash generation has remained very strong and valuations are highly compelling. We are drawn to companies like Unilever that are - as with Howden - controlling the controllables to drive growth through and beyond this difficult period for the global consumer.

In March, Unilever announced the combination of its Foods business with McCormick, creating a global leader in flavours and condiments with brands including Knorr, Hellmann’s, McCormick herbs and spices, French’s mustard and Frank’s RedHot Sauce. The valuation achieved was above market expectations at around $45bn enterprise value, representing a higher multiple than Unilever itself currently trades on, despite Foods being a lower-growth business. Unilever shareholders will receive around 65% of the combined company’s equity, plus a $15.7bn cash payment.

The market’s initial reaction was negative. Some complexity to the Unilever investment case is introduced until the deal closes in mid-2027, and there may be selling pressure from investors who are unable or unwilling to hold a US-listed food business. These are understandable short-term concerns, and events in the Middle East have also weighed on sentiment towards all consumer names over the last month.

In our view, the more important perspective for the long-term shareholder is that this deal completes Unilever’s multi-year transformation into a focused Home and Personal Care (HPC) business. Standalone Unilever will be built around Beauty, Wellbeing, Personal Care and Home Care, with structurally higher gross margins of c.48% and management targeting +4-6% organic revenue growth over the medium term. Cash from the transaction will be used to reduce debt and return €6bn to shareholders through buybacks by 2029. At around 15x earnings - compared to 21x for its global HPC peers - the valuation looks very attractive for a business with a significantly improved growth and margin profile. The dividend yieldii and free cash flow yieldiii stand at 4% and 6.2% respectively.

Hugh, Chris M., Ben P., Charlotte, Leon and the Evenlode team

22 April 2026

Evenlode has developed a Glossary to assist investors to better understand commonly used terms.

Market data is sourced from S&P Capital IQ, Financial Express Analytics and Bloomberg unless otherwise stated.

This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject to change and are not guaranteed.

IFSL Evenlode Income is a sub-fund of the IFSL Evenlode Investment Funds ICVC. Full details of the Evenlode Funds, including risk warnings, are published in the IFSL Evenlode Investment Funds Prospectus and the IFSL Evenlode Investment Funds Key Investor Information Documents (KIIDs) which are available on request and at www.evenlodeinvestment.com.

The IFSL Evenlode Investment Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, IFSL Evenlode Income may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

FTSE® is a trademark of the relevant London Stock Exchange Group plc (“LSE Group”) companies and is used under licence. FTSE Russell is a trading name of certain LSE Group companies. All rights in FTSE Russell indices and data vest in the relevant LSE Group company. Neither LSE Group nor its licensors accept any liability for errors or omissions in the indices or data, and no reliance should be placed on this information. Redistribution of LSE Group data is prohibited without prior written consent. LSE Group does not promote, sponsor, or endorse the content of this communication.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited (IFSL) is authorised and regulated by the Financial Conduct Authority, No. 464193.

Footnotes

-

Source: FE Analytics and Evenlode as at 22 April 2026.

-

Dividend Yield - Dividend payment made by a company to shareholders, expressed as a percentage of the share price.

-

Free Cash Flow (FCF) per share divided by the current share price. A higher Free Cash Flow Yield implies a company is generating more cash that could be paid out as dividends and to reinvest into growth of the business. The Free Cash Flow Yield for a portfolio is the total free cash flow generated by a portfolio, divided by the market value of the companies in the portfolio.

-

Median organic growth rate for all portfolio holdings. Revenue and organic operating profit figures do not include FX or M & A impact. Calendar year numbers for all holdings (adjustments are made for companies whose financial year end is not December). Source: Visible Alpha, S&P Capital IQ, Evenlode Calculations. April 2026.

-

P/E Ratio - A measure of a company’s current market valuation compared to its earning potential, calculated by dividing a company’s share price by its Earnings per share (EPS).