After the war-related sell-off in March, global stock markets recovered in the second quarter with company earnings remaining robust, a ceasefire deal between the US and Iran agreed, and the oil price falling rapidly back towards pre-conflict levels.

Share price volatility versus fundamentals

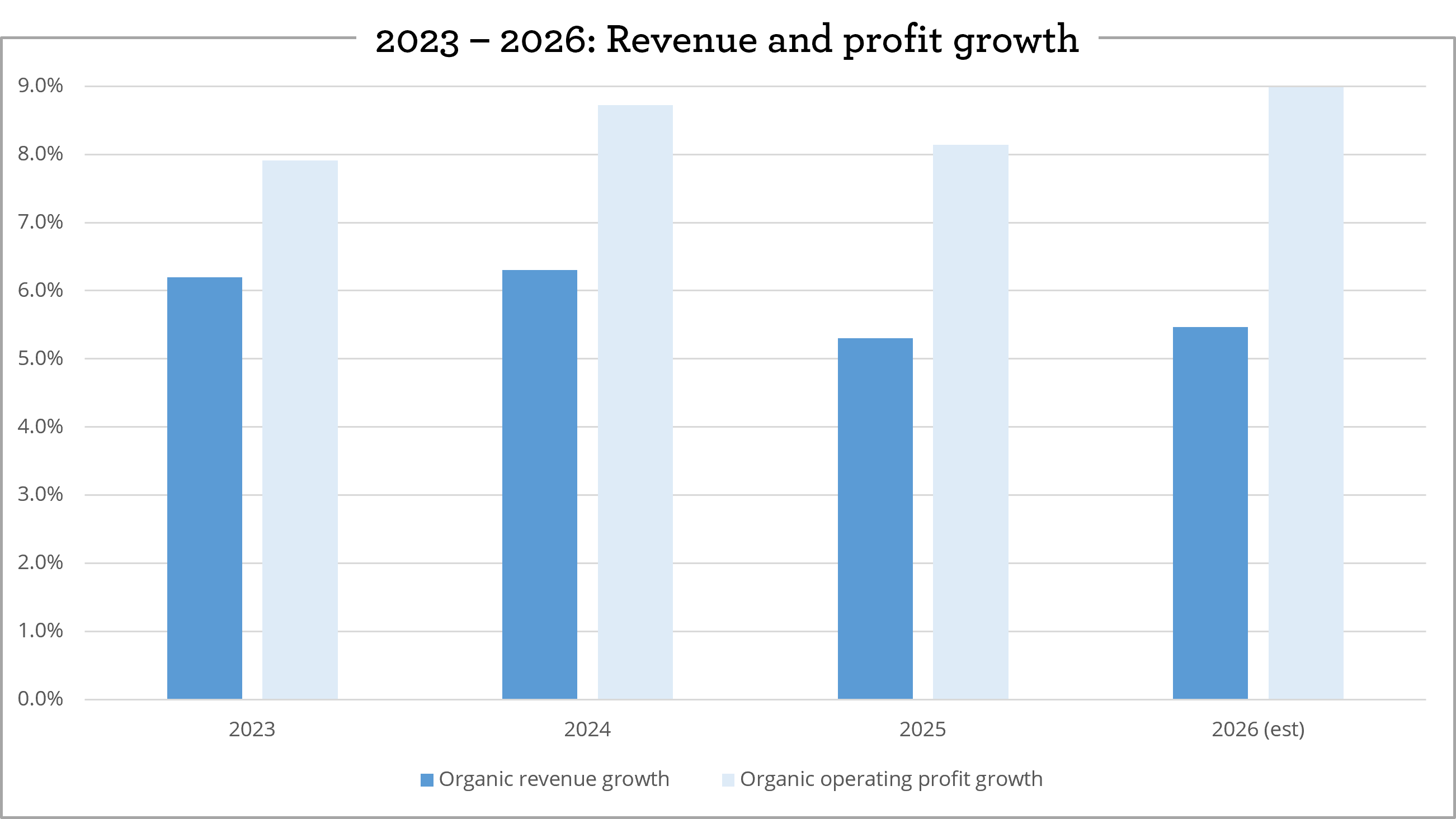

Taken as a whole, IFSL Evenlode Income’s unit price has fallen -0.8% year-to-date, with unusually high share price volatility for IFSL Evenlode Income holdings during the six-month period.i This volatility is in stark contrast to the fundamental performance of underlying holdings, which continue to generate strong free cash flow and are growing revenues and profit at a good rate in aggregate. The below chart shows the organic revenue and operating profit growth for portfolio holdings over the last three years and the expectation for growth in 2026.

Median organic growth rate for all portfolio holdings. Revenue and organic operating profit figures do not include FX or M & A impact. Calendar year numbers for all holdings (adjustments are made for companies whose financial year end is not December). Source: Visible Alpha, S&P Capital IQ, Evenlode Calculations. April 2026.

The 2026 forecasts (i.e. the two bars at the right of the chart) stand at a very similar level to where they stood in early January. The expectation is for more than +5% organic revenue growthii, +8% organic operating profit growthiii, and double-digit earnings per share growthiv.

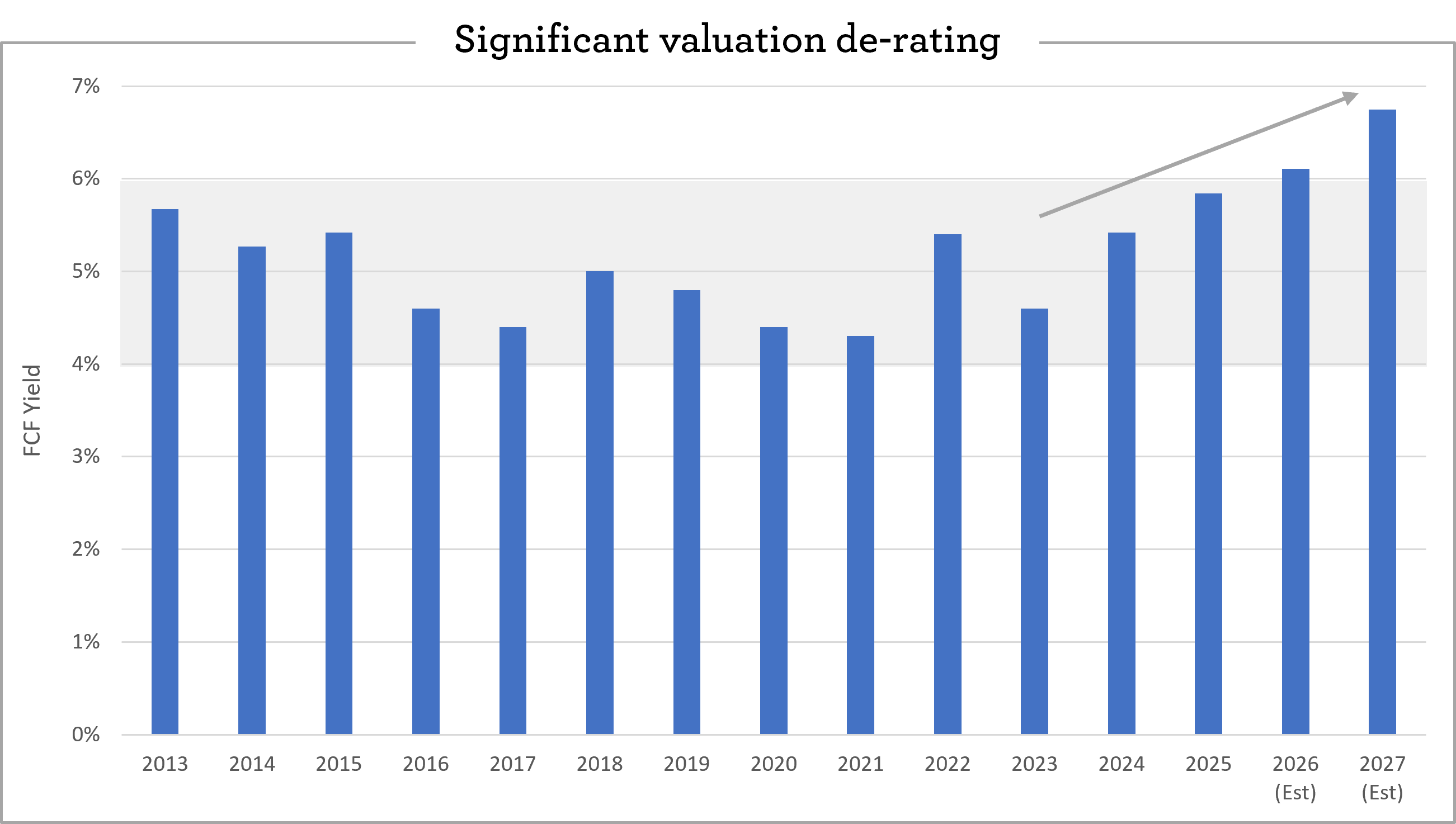

Most attractive valuation since the early days of the fund

UK-listed quality shares have been very out of favour over the past two years, with UK market returns concentrated in asset-intensive cyclicals - most notably banks and resources companies. Meanwhile, the US market (and the global market by proxy) has become concentrated in and dominated by the AI capital investment trade. Trends are very polarised, with the momentum factor having its strongest run in global markets since the 1999-2000 period.

The below chart shows IFSL Evenlode Income’s recent valuation de-rating in terms of the rise in free cash flow yieldv - a key valuation measure for us. Remarkedly, the free cash flow yield on the fund is more attractive than it was even in the depths of the Covid sell-off in 2020 and is back to a similar level to the fund’s launch in October 2009, when the world was emerging from the Great Financial Crisis.

Source: Evenlode, 30 June 2026.

Despite the competitive advantages, growth potential and capital-efficient economics these companies enjoy, the portfolio’s free cash flow yield is currently higher than the FTSE All-Share Index and nearly twice as high as the MSCI World Index.

Mathematically - as laid out in the ‘Geek’s Note’ appendix to this piece - the capital-efficient economics of the companies in the portfolio should lead them to trade at a significant premium to the average company. Their current discount to market averages is therefore a highly unusual situation that I expect to mean revert over time.

Over the last couple of weeks, there are some very early signs that the stock market may be beginning to broaden out - both within the UK and global markets. If this trend continues it would be very helpful for the fund. I would also note that on a fundamental basis, the cessation of all-out war in the Middle East and the resultant drop in the oil price will be a helpful tailwind for a range of holdings as it feeds through to lower interest rate expectations (helpful for demand) and lower input costs (helpful for profitability).

Field notes from the portfolio

The last few weeks have been relatively quiet for fundamental news-flow, but we have had plenty of engagement with companies. For the rest of this view, I will update on two holdings that have had news out over the last month - Howden Joinery and Experian - and then finish with some observations on generative AI adoption in the corporate sector, following the many conversations we have had with management teams on the topic over recent weeks.

Howden Joinery

Howden Joinery announced the acquisition of DIY Kitchens earlier this month. It’s not a bet the house acquisition, with the £390m purchase price representing 9% of Howden’s £4.3bn market capitalisation, but it is strategically significant. Howden has developed a very strong position in the UK kitchen market, with consistent share gains since it separated from MFI two decades ago, and now has a market share of around 25%. Howden is exclusively focused on serving the trade channel – selling kitchen and joinery products to local trade builders. The trade channel represents around a quarter of the UK kitchen market; Howden is effectively the market in this segment! Its vertically integrated in-stock model, well-invested product range and nearly 900 UK depots providing a high-touch service to local trade builders has proven very hard to compete with. However, Howden doesn’t sell directly to consumers, and direct-to-consumer (DTC) represents around two-thirds of the UK kitchen market, consisting mainly of bricks-and-mortar retailers such as B&Q and Wren, and smaller independents.

DIY Kitchens gives Howden an additional route to market and expands its accessible customer base. It sells kitchens directly to consumers via its website, supported by two large destination showrooms, and manufacturing facilities, with around 40% of cost-of-goods (COGS ) manufactured in-house, a similar level to Howden. It provides consumers with self-service planning, design and ordering tools. The proposition is winning share in the market, with revenue growing at 17% per annum over the past 5 years. With penetration low – it has a 1-2% market share - management expect to continue compounding revenue at a double-digit rate.

Unlike most of its competitors, it doesn’t have a high-street branch network, and customers prepay for made to order product, giving it a very attractive margin and cash flow profile – its EBITvi margin of 27% in 2025 compares to Howden’s 15%. The business will be operated separately from Howden, but there may be scope for material savings in manufacturing and procurement over time. For a strategically significant, high growth, high margin business, the valuation looks attractive, with Howden paying slightly less than its own valuation for the company.

We think Howdens’ investment case and valuation are compelling, trading on a Price-to-Earnings (PE) ratiovii of 15x and free cash flow yield of 6%, and we have been adding to the position in recent weeks. Even with this acquisition, and the continuation of the current £100m share buyback programme, the business will continue to operate with a net cash balance sheet. In recent years Howden has delivered growth despite a subdued market environment, with UK kitchen volumes last year more than 20% below the long-term average, and lower than the 2009 trough. We think pent up demand is building, and the recent fall in the oil price is also directionally positive for the UK interest rate outlook - a helpful incremental tailwind. In a scenario where market volumes revert to historical average levels, Howden’s earnings could easily double over coming years, even before the contribution from DIY Kitchens. If a market recovery doesn’t materialise, we still think Howden can deliver attractive growth, with scope for continued share gains and depot expansion in the UK, along with opportunities to significantly expand penetration with DIY Kitchens and its less mature businesses in Ireland and France.

Experian

Information services companies have been some of the fund’s most negative contributors to return this year. They make up approximately 15% of the portfolio with RELX, Experian and LSEG the main holdings. Though fundamental performance has been good, they have seen a heavy valuation de-rating driven by concerns that AI could disintermediate their relationships with clients.

We attended an Experian investor briefing in June. The company addressed these charges head on, presenting the opportunities it sees ahead and demonstrating the generative AI tools developed thus far. Experian believes generative AI could expand its North America addressable market to $115bn, up from $100bn, with a further $15bn+ of newer opportunities identified on a 2030 basis. While the opportunity is wide-ranging, the demonstration of two new services stood out.

The first was the Agent Operating System (AOS), which extends their Ascend platform - used by all major US banks to decide whether to offer credit to individuals. AOS adds model oversight and monitoring to Experian's existing platform and lets banks deploy agents that map to recognisable job roles in credit risk, fraud, marketing and governance. The demonstration was impressive; human-in-the-loop approval, an immutable audit trail and automated compliance checks are all built in, which speaks directly to the trust concerns that are acting as barriers to AI adoption. As a trusted partner that already integrates high value credit data with the bank’s own data, Experian are well placed to offer this service and there is little incentive for banks to build these services themselves. Experian report a return on investment of over 150% for banks employing the system thus far. Management plan an incremental rollout, with processes moving from manually approved to AI-enabled at a tailored speed to suit each client.

The second new service, Agent Trust, is at an earlier stage. As consumers begin to delegate purchases to AI shopping agents, merchants need to know that an agent is genuine and acting for a real, creditworthy individual. Experian verifies the agent and binds it to a person, so the merchant can transact with confidence. This complements merchant-side verification being built by Google and Shopify rather than competing with it. Experian has assembled a coalition including the major language models and Visa, with Mastercard expected to follow. This combined coalition would cover roughly 90% of ecommerce transactions. The barrier to adoption here is threefold. First, consumers need to shift to agentic commerce, which has failed to take significant share thus far. Second, vendors need to build this into their checkout systems. Third, the payment mechanism needs to be agreed. It is likely that an extra fee from the vendor (similar to the interchange fee on card transactions) would be unpopular.

Both are examples of a company investing heavily to harness generative AI for growth in new emergent markets. Experian’s investment case, though, does not rest on these newer markets maturing. The company’s proprietary and contributory datasets remain a very strong economic moat, and management is on the front-foot –viii as usual - in terms of investing for growth within its existing business lines. This includes harnessing generative AI technology to both enhance and expand its products and also increase operational efficiency. The stock currently offers a combined dividend and buyback yield of over 5%, and analyst consensus forecasts double-digit profit growth over each of the next three years. A re-rating would further help returns, and the Experian management team’s willingness to invest is key to demonstrating the substantial upside from generative AI technology. The stock currently trades on a next-twelve-month Price-to-Earnings multiple of 16x and a free cash flow yield of 6.4%. This is the lowest valuation the company has traded on for over a decade.

Reflections on generative AI adoption in the corporate sector

I will finish this piece with some broader reflections on generative AI adoption in the corporate sector, following a host of conversations with both UK and global companies.

My headline summary is as follows:

- Point 1: Generative AI is a very powerful technology, of transformational benefit in some areas and of less relevance in others.

- Point 2: The process of diffusion (the widespread use of AI by businesses in everyday tasks) is at an early stage – with diffusion in software engineering teams most advanced. The overall process will unfold over time.

- Point 3: Most management teams – mainly due to the broader digitalisation and automation trends of recent years, but also in light of generative AI - expect to grow revenue and profits at a significantly faster rate than their workforce will grow.

- Point 4: Corporates are moving from ‘tokenmaxxing’ (using AI models as much as possible) to ‘valuemaxxing’ (shifting the focus from volume of use to measurable value).

- Point 5: The provision of basic AI computeviii and model access is commoditising rapidly for most standard inference needs.

Let’s discuss each of these points in a little more detail:

Point 1: Generative AI is a very powerful technology, of transformational benefit in some areas and of less relevance in others.

First, a couple of caveats:

- Given their probabilistic underpinnings, Large Language Models (LLMs) are inherently unreliable. They are not good at performing deterministic tasks that absolutely need to be 100% correct.

- The performance improvements of the latest frontier LLM models are beginning to slow as they have now had the entire Common Crawl (i.e. the whole of the internet) thrown at them as training data.

With that said, though, the technology is genuinely transformational. It is – as we are finding at Evenlode - a very good search, research and brainstorming tool. It’s particularly good at compressive analysis (i.e. processing and summarising a large body of work).

It has also found its ‘killer app’ in software coding this year thanks to Claude Code and similar AI coding tools. The big innovation with these tools is the use of a deterministic orchestration layer (or ‘harness’). These harnesses integrate deterministic algorithms with the LLMs’ probabilistic approach, making them more reliable (though LLMs can never be 100% reliable, even with a harness). A good analogy for the harness is that they act like a nanny keeping an errant child in check!

‘Agentic AI’ is the concept of sending these harnessed LLMs off to perform tasks on one’s behalf. The Experian section above touches on one potential use case for Agentic AI in online commerce.

Point 2: The process of diffusion is at an early stage, with diffusion in software engineering teams most advanced. The overall process will unfold over time.

One of the bibles of new technology transitions is Carlota Perez’s Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages (2002). One of Perez’s key observations is that the diffusion of new transformational technology takes time, due as much to the need for institutions, society and skills to adapt, as much as the technology itself.

Technology analyst Benedict Evans makes a similar point on generative AI deployment:

“This isn't something that any big company does quickly - it takes time even to work out what you might want to do; it involves a lot of work in working out what the process should be and then going out and plugging it all together. That creates a paradox, if you like, that automation requires a lot of manual labour.”

In terms of the current wave of generative AI diffusion, search and software engineering have been leading the way. Most companies with software engineering teams think they will achieve coding efficiency gains of between 10-30% over time from AI coding tools. This is not necessarily what they are achieving now, but what they think they can achieve once they have fully embedded the new technology, and re-engineered workflow and job roles around the new technology.

Other uses of generative AI are being trialled and deployed across a variety of use cases – within research and analytical functions, content creation, finance, legal, customer support, administration, and social media, advertising and marketing optimisation. As with software engineering, efficiency gains are beginning to come through. Meaningful diffusion is taking time though, and corporates are also nervous about the inherently unreliable nature of LLMs. This is especially true when the cost of being wrong is very high - in highly regulated, mission-critical areas. Corporates also worry about copyright infringement and their own data privacy. For some areas of the corporate workflow - where only 100% reliable, deterministic algorithms will do - LLMs are simply not relevant and very ill-suited to the task.

Point 3: Most management teams – mainly due to broader digitalisation and automation trends of recent years but also in light of generative AI - are aiming to grow revenue and profits at a significantly faster rate than their workforce will grow.

There have been some news headlines about big job cuts at large corporates over recent months. This has been skewed towards the big US technology companies themselves - which hired heavily in the Covid period - and more structurally challenged industries such as the European automotive sector.

We are hearing a more nuanced picture on the ground with respect to AI’s impact on corporate employment. Big job reductions aren’t the norm, but most management teams are seeing the potential for labour-efficient growth over coming years. First, thanks to the broader digitalisation trends that have been ongoing for more than a decade. Second, thanks to generative AI benefits such as more productive software engineers. Experian, for instance, have grown earnings at more than +10% per annum over the last two years with no change in the company’s net headcount, and expect a similar trend over coming years. Financial platform provider Integrafin has been steadily driving more automation into its workflows. This has reduced the need for headcount and cost growth. During the first half of 2026, revenues rose +11% and profit before tax rose +16%.

Point 4: Corporates are moving from ‘tokenmaxxing’ to ‘valuemaxxing’.

“If you’re not actually able to draw a direct line to how many useful features and functionality you’re shipping to your users, the expense becomes harder to justify because AI is not free".

Uber CEO – May 2026 (after burning annual AI token budget in 4 months!)

“Our software engineers come to me and say ‘I want to use Claude Code because it’s the best’. And I’m saying to them ‘well, I know Claude Code is the best. But the open weight models are not far off now in terms of performance, and they are a fifteenth or a twentieth of the cost. I understand that in certain use cases it makes sense to use the frontier models, but for the majority of our inference tasks, using the open weight models through open-router services makes huge economic sense".

CFO, FTSE 350 company, Evenlode 1-2-1 Meeting – June 2026

“The vibe-coding market is in the process of heavy commoditisation".

Technology Expert, Evenlode Interview – June 2026

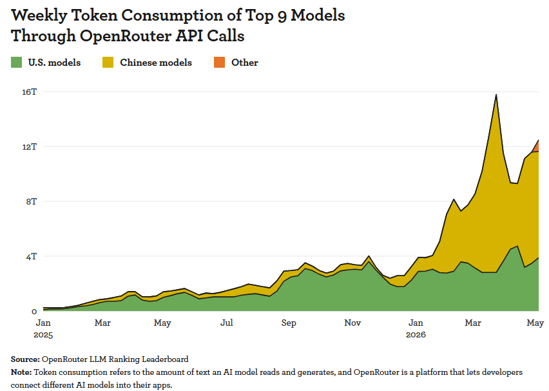

There was much press coverage of the ‘tokenmaxxing’ mania that lasted for most of April and May and included internal leaderboards for individual employees at large US corporates such as Meta and Amazon recording who was spending the largest amount of money on tokens. This culminated in the news that one large US company (rumoured to be Amazon) managed to burn through $500m worth of AI tokens using Claude – in a single month! That would be $6bn at an annual rate!

As the quote above from a FTSE 350 CFO suggests, finance departments are now stepping in and scrutinising the cost/benefit of token spending. The expenditure has not suddenly led to a dramatic increase in revenues or a dramatic increase in efficiency – gains have been at the increment. Meanwhile, a host of lower cost alternatives to the frontier models are emerging. ‘Open-weight’ and ‘open-source’ models – many but not all from China – are rapidly catching up on performance versus frontier models, are less compute-intensive, and are available at a fraction of the price. Companies are also turning to AI router systems, such as OpenRouter. These services route AI compute requests to a growing number of providers, and optimise based on performance, cost and availability of compute. This trend has led to an explosion in the usage of open-weight models over the last few weeks.

Point 5: The provision of basic compute and model access is therefore commoditising rapidly for most standard inference needs.

This shift to lower cost models is well illustrated in the below chart (many, but not all, of the open weight models are Chinese).

Competitive pressures in the LLM model access market are therefore growing fast – as demonstrated by the mid-June news story that the heavily loss-making OpenAI is considering big price cuts in an attempt to stay competitive and keep its usage numbers growing ahead of a potential IPO – which subsequently appears to have been put on hold.

This is a commoditising and heavily capital-intensive sector. This duo of characteristics raises questions over what return on investment may ultimately be generated from the huge capital stock that is building up within the US hyperscale datacentre sector.

These questions, though, are of more relevance to global investors than the average company management team. From a corporate perspective, the key questions management are asking themselves of generative AI are as follows:

- How can we harness this new technology to enhance our services and improve efficiency?

- How do we need to reorganise teams and their workflows to get the most out of it?

- What are the regulatory, legal and reputational risks we need to manage?

- How can we get value for money, and how can we ensure that the returns on investment are compelling?

There are no shortage of enterprises busily figuring out the answers to these questions, whilst also possessing durable competitive advantages and capital-efficient economics. Many are trading on unusually attractive valuations as global investors have shunned them in favour of those stocks most exposed to the US datacentre build-out.

We would like to thank our investors for their patience and continued support through a difficult first half of the year. We remain confident in the quality of the businesses held in the fund and believe the strategy is very well placed to reward patient capital over time.

Hugh, Chris M., Ben P., Charlotte, Leon and the Evenlode team

6 July 2026

Appendix - Geek’s Note:

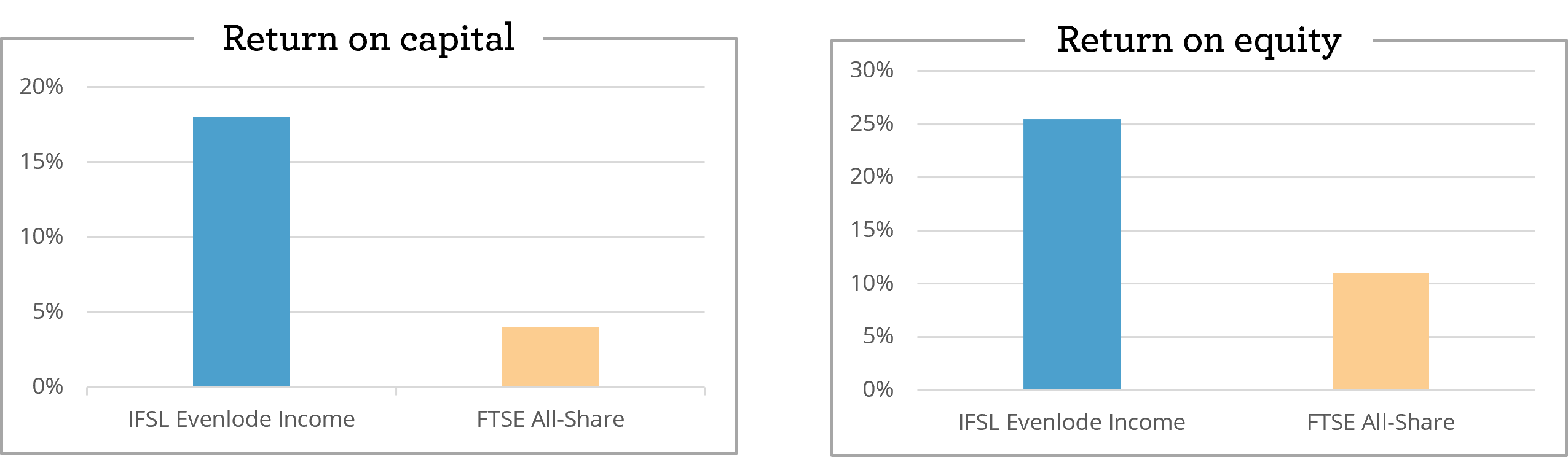

Let’s assume two companies, where Company A is able to generate growth with twice the capital efficiency (i.e. twice the incremental ROIC) as Company B: 20% for Company A compared to 10% for Company B.

Company A has to invest £35 in every £100 to generate 7% growth (£35*20%), leaving £65 for distribution but Company B has to invest £70 to generate the same 7% growth (£70 *10%), leaving only £30 for distribution.

For the net present value of each company’s cash-flows to be the same, Company A needs to trade at a Price-to-Earnings (PE) multiple of more than twice that of Company B.

For instance, let’s assume a 10% cost of capital for both businesses. Assuming a 7% earnings growth for both companies as above, Company A should trade on a fair value PE multiple of 21.7x (0.65 / [0.10- 0.07]) and company B should trade on a PE multiple of 10x (0.30/ [0.10-0.07]).

In other words, not all growth is equal. Capital-efficient growth should be valued more highly than capital-intensive growth. But in the current market it is not. The below chart shows the Return-on-Capital and Return-on-Equity of the IFSL Evenlode Income portfolio compared to the FTSE All-Share. As mentioned in the main section of the piece, the current free cash flow yield for the portfolio is currently higher than the UK market and more than twice as high as the global market

Source: Evenlode, Bloomberg, 2026.

Important information

Evenlode has developed a Glossary to assist investors to better understand commonly used terms.

Market data is sourced from S&P Capital IQ, Financial Express Analytics and Bloomberg unless otherwise stated.

This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject to change and are not guaranteed.

IFSL Evenlode Income is a sub-fund of the IFSL Evenlode Investment Funds ICVC. Full details of the Evenlode Funds, including risk warnings, are published in the IFSL Evenlode Investment Funds Prospectus and the IFSL Evenlode Investment Funds Key Investor Information Documents (KIIDs) which are available on request and at www.evenlodeinvestment.com.

The IFSL Evenlode Investment Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, IFSL Evenlode Income may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

FTSE® is a trademark of the relevant London Stock Exchange Group plc (“LSE Group”) companies and is used under licence. FTSE Russell is a trading name of certain LSE Group companies. All rights in FTSE Russell indices and data vest in the relevant LSE Group company. Neither LSE Group nor its licensors accept any liability for errors or omissions in the indices or data, and no reliance should be placed on this information. Redistribution of LSE Group data is prohibited without prior written consent. LSE Group does not promote, sponsor, or endorse the content of this communication.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited (IFSL) is authorised and regulated by the Financial Conduct Authority, No. 464193.

Footnotes

-

Source: Financial Express, to 6 July 2026, B Acc.

-

Organic Revenue Growth – The percentage increase of sales generated from a company’s existing resources and operations. Excludes growth attributable to mergers and acquisitions and foreign exchange.

-

Organic Operating Growth – The percentage increase of earnings derived from a company’s existing operations. Excludes growth attributable to mergers and acquisitions and foreign exchange.

-

Earnings Per Share (EPS) - A measure of company profitability, calculated by dividing a company’s profit by the number of shares in issue.

-

Free Cash Flow Yield - Free Cash Flow (FCF) per share divided by the current share price. A higher Free Cash Flow Yield implies a company is generating more cash that could be paid out as dividends and to reinvest into growth of the business.

-

EBIT – Earnings before interest and taxation.

-

Price Earnings Ratio - A measure of a company’s current market valuation compared to its earning potential, calculated by dividing a company’s share price by its Earnings per share (EPS).

-

Compute – The computing power required to support AI models – chips, data centres, memory, power, network resources etc.