Introduction

Coffee and cocoa are luxury ingredients which were commoditised through colonialism and the slave trade. From the 15th century this commoditisation has occurred at the expense of people and the environment, resulting in forced labour, child labour, mass deforestation, loss of biodiversity and destruction of soil quality.

This has led to structural issues causing extreme price volatility in the coffee and cocoa futures market over the last three years. In order to manage the commodity price volatility, companies who sell products containing the ingredients of coffee and cocoa have passed the increased input cost onto the customer; this illustrates that structural issues upstream have a direct consequence on the downstream consumers.

Premium companies and brands such as Lindt & Sprüngli and Nespresso can optimise on coffee and cocoa becoming luxury ingredients for the consumer. This means that they are well positioned to manage the fundamental change in approach or ‘paradigm shift’ within the industry compared to those who have treated these commodities as staples.

The following white paper will discuss the development of social and environmental structural issues which are driving the paradigm shift in both coffee and cocoa. The companies which are exposed to these ingredients in Evenlode’s portfolios will then be addressed, before concluding on the financial implications for the companies and investors, and what can be done to stabilise the coffee and cocoa industry.

1. Coffee

1.1: The history and geography of coffee

To understand the issues currently facing the coffee market we must look to the past.

The coffee plant is native to Ethiopia but began its globalisation in the 15th century when it was transported to Yemen, where it was cultivated and traded for the first time. Yemen controlled the crop throughout the Ottoman Empire and traded it throughout the middle east as a luxury beverage. However, Dutch traders smuggled coffee from Mocha in 1616, and this marked the beginning of European colonisation of coffee.i

Coffee gained significant popularity throughout Europe during the enlightenment period (1685-1815) due to its association with wisdomii and the development of the ‘Coffee House’. The Dutch East and West India companies led the commoditisation of coffee, using their developed nautical transport systems and established slave trade routes. By 1690, the Dutch had set up coffee plantations in Java, Celebes, Timor, Bali and Sumatra. The monopolisation of the Dutch and the success of coffee as a traded commodity drove other European colonial powers to compete for market share throughout the 17th century, all while exploiting the land and labour on which coffee was being produced. This included the development of coffee plantations in Saint-Domingue (Haiti) in 1734 which, by the 1780s, was producing over half of the global coffee supply due to the extreme practices of slave labour.iii

As demand in Europe grew, the price of coffee dropped due to slavery and exploitation of land in the colonies. Coffee became accessible to all, and it was no longer considered a luxury. Finally, the increased tax placed on tea by the British led to the Boston Tea Party in 1773 and coffee became the morning beverage of choice throughout the colonies, thus creating further demand.iv

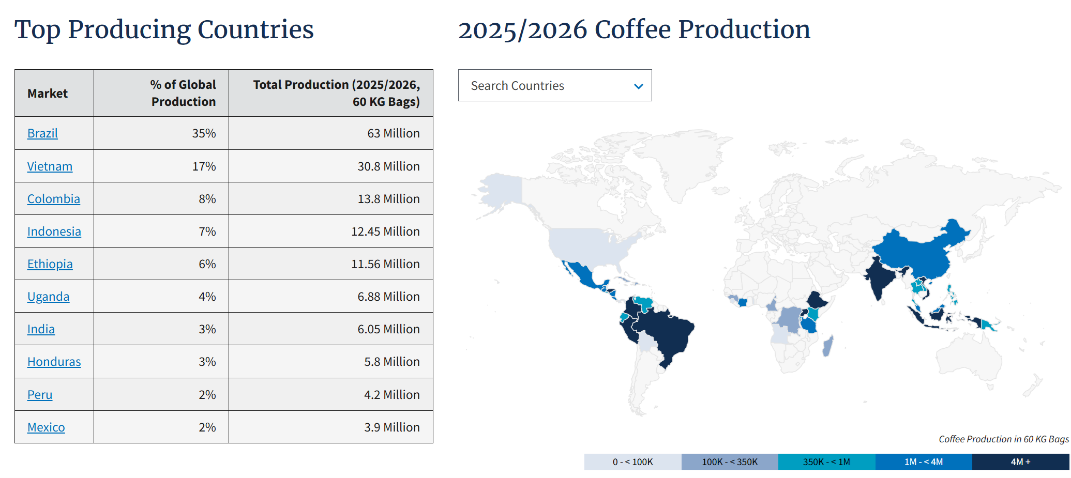

The most significant migration of Coffee, via colonialism, was into Brazil in 1727.v The crop thrived, and by the 1830’s, Brazil was producing a third of the world’s coffee. This remains the case today with the country supplying 37% of global demand in 2024/2025.vi

1.2 Structural issues coming home to roost

Through the heavy colonisation and commoditisation of coffee, people and land have been abused to support the corporate margin dynamics investors look for. This has led to structural issues in both the social and environmental supply chain. For this report, the focus will be on Brazil as the dominant source of coffee worldwide.

Structural social issues

The social issues associated with coffee, stem from the history of slavery and indentured labour. Unfortunately, many of these practices are still in place. The coffee supply chain contains human rights violations such as forced labour, child labour, wage theft and payments under the minimum wage. These issues are embedded into the supply chain, and it would be near impossible to purchase and consume coffee without one of these factors being part of the final product. This is due to mass balance sourcing where all small holder coffee will enter the manufacturing process without clear traceability to the original farm and farmer. Around 95% of coffee farms are smaller than five hectares but combined they produce three quarters of the world’s coffee.vii

Forced labour is the most material social issue in the coffee supply chain. This includes debt bondage, excessive working hours, degrading accommodation and food, and lack of payment. There have been multiple class action lawsuits against Starbucks - not an Evenlode investee company - where workers were unpaid, operating without protective equipment and working for over twelve hours without breaks.viii Trafficking workers, who are often children, and subjecting them to slavery-like conditions is the foundation of the Brazilian coffee supply chain and the coffee sector has the highest number of workers rescued from slavery-like-conditions in Brazil.ix/x/xi

Not only is slavery morally abhorrent, it creates unstable supply chains and exposes companies to significant litigation risk. Companies are complicit in slavery via the supply chain, either by not paying enough for the product they are buying, not conducting appropriate due diligence or not engaging with their suppliers sufficiently.

Structural environmental issues

Coffee, in Brazil and elsewhere, has become a paradoxical crop. The deforestation required to grow and expand coffee has caused a change in the microclimate and reduced the coffee yield, therefore deforestation is causing the demise of the coffee crop. Direct deforestation and indirect deforestation relating to coffee, has decimated the forests in the southeast of Brazil known as ‘the coffee belt’.[6] According to Coffee Watch, ‘the growth [of coffee] was powered by railroads, propped up by slave labour, and fuelled by global consumption’.xii

Coffee is an incredibly sensitive crop, requiring a specific climate, soil nutrition, rainfall and altitude. The Atlantic Forest in Brazil provides all these elements for coffee and is the key factor to coffee’s success in Brazil. The flourishing of the crop in Brazil, along with the ever-increasing demand for the beverage in Europe and America, led to Brazil producing 30% of global coffee in 1830 to over 80% of the world’s coffee by the 1930s. With the Minas Gerais region of Brazil producing more coffee than entire countries such as Panama.xiii

However, as coffee is not native to Brazil, deforestation is needed to create land on which coffee can be cultivated. As a result, only 12.4% of the original Atlantic Forest remains, leading to a significant impact on the microclimate coffee requires for growth.xiv This is primarily seen in the rains of Brazil. Coffee requires a specific amount of rain between January and March when the beans are formed and the quality of the harvest is determined.xv Too little rain will significantly impact the yield and quality of the harvest. This is primarily due to the negative impact it has on soil hydration; the plants cannot gain the nutrients from the soil needed to produce high quality beans. It is like asking someone to run a marathon without water - it is not going to perform well.

Finally, the issues of deforestation and inconsistent rain have led to the increase of disease and pests on coffee crops such as Coffee Rust. These diseases have historically been managed by the avian population of the canopies that coffee is grown under. However, with the lack of canopies in place, the population of birds is not present to manage the pests. The development of growing coffee in a monoculture and in full sun means that using pesticide is now essential to protect the crop and yield; this damages the quality of the soil further and poses significant health risks to the small holder farmers.

The demand for coffee continues to grow. Over the last decade, demand for coffee in China has increased 150% and is up 15% since 2024, compared to the 2.2% increase witnessed globally.xvi However, the data shows that coffee supply could halve by 2050 - particularly for the Arabica Bean.xvii In Brazil, this coffee loss would be up to two thirds of the crop, due to the intensity of the climate-related issues and vulnerability of the crop.[13] The demise of the coffee crop will have significant financial implications for Nestlé, the largest buyer and seller of coffee in the world.xviii

This is a structural environmental problem which is causing a negative feedback loop. Aggressive deforestation and industrialisation by the coffee industry have driven drought, poor soil quality and disease. This results in poor yields, which in turn drives further deforestation in order to maintain the supply to meet the growing demand for coffee.

1.3 So what?

There are a myriad of problems relating to coffee, but what does this mean for investee companies and what can be done to strengthen the supply chain thus reducing the risks associated with coffee production?

1.3.1 Nestlé

Evenlode’s primary exposure to the coffee supply chain sits with Nestlé which is held in IFSL Evenlode Global Income (EGI). At the time of writing, Nestlé is held at 3.5% in EGI. The ‘Powdered and Liquid Beverage’ segment of Nestlé makes up 27% of revenue and operating profit. The majority of this is accounted to coffee with Nespresso making up circa 7% of this segment. Therefore, coffee makes up circa 1% of the EGI Portfolio. However, there is wider exposure via Diageo and Pernod Ricard who sell coffee liqueur.

1.3.2 How can we reduce the risk associated with the coffee supply chain?

Shareholders, such as Evenlode, are the most long-term stakeholders in a company such as Nestlé. Company executives are responsible for quarterly and annual performance, but they are unlikely to be held responsible for the coffee yield halving by 2050. There is a misalignment between C-suite executive incentives and investors who are committed to the long-term success of the business. According to Etelle Higonnet, the CEO of Coffee Watchxix: ‘Investors need to push companies to increase resilience in the coffee supply chain, but investors must be comfortable with the short-term margin impacts this will have. This will ensure the long-term performance and safety of the crop’. The short-term pain of securing the coffee supply chain for the future will include the transition to regenerative agriculture and crop resilience, please see Sawan Wadha’s white paper on regenerative agriculture for more detail on this.

1.3.3 What is the change that the investors should be asking for from the C-suite?

Coffee Watch suggests that the first steps companies need to take is to acknowledge the scale of deforestation before restoring the ecosystem and transitioning towards regenerative agriculture.

Currently only 1% of Brazilian coffee is grown in regions using agroforestry (combining agriculture with trees)xx. Without large scale agroforestry, Brazil risks economic decline, stranded assets and exclusions from key markets such as the EU with the inclusion of European Union Deforestation Regulation (EUDR).xxi Furthermore, there is a complete lack of funding for agroforestry. As discussed, those working on the farms are often working in slavery-like conditions and the supply chain is dominated by small holder farmers (84% in Brazil) which means that they struggle to earn a living wage.xxii To add to this, the coffee price is extremely volatile; for example, following the drought between 2016 and 2019, the coffee price fell significantly and pushed many farmers and communities into deeper poverty. The rising production costs of coffee due to tariffs, EUDR and erratic weather patterns - like drought and frost - across Latin America are exacerbating this poverty further. Higher rates of poverty lead to an increased reliance on forced and child labour. When this is the context coffee farmers are working within, regenerative agriculture cannot be a priority when it requires significant initial capital outlay with no guarantee of increased yield over the short-term.

The structural social and environmental issues within the supply chain come down to unfair value distribution. The commodity price increases are managed by the roasters, traders and retailers and to protect margins, the cost is passed onto the consumers. The farmers, however, gain very little for their work and the consolidation at the top of the supply chain between major brands (Nestlé, JDE Peets BV, Starbucks, Lavazza)xxiii only skews this unfair value distribution further. When this is coupled with drought and increased disease, thus reducing yield, the outlook is bleak for coffee farmers.

As shareholders we need to ensure that the companies who are procuring the coffee are paying farmers the right price to ensure the value is distributed more equally. This will allow companies and farmers to invest in regenerative agriculture, which will safeguard their yield for the future and ensure resilience in the coffee supply chain on a wider level. Investors might have to accept a short-term impairment to gross margins resulting from an increase in cost of goods sold (COGS) to help facilitate top line growth over the long term.

Nestlé has done multiple pilot projects involving regenerative agriculture through the Nespresso AAA Sustainable Quality Program. However, they are yet to successfully scale this. The new CEO of Nestlé was the previous CEO of Nespresso where they prioritised the sustainability of the coffee they procured. This change in management at Nestlé will hopefully lead to a prioritisation of increasing coffee supply chain resilience. This can be done by passing financing to the farmer and ensuring the process of regenerative agriculture is de-risked as much as possible.

If Nestlé’s shareholders and executives are aligned in the view that the sustainability of coffee is a key business risk, upstream supply chain dynamics should improve. Fairer distribution of value will allow farmers to transition to regenerative agricultural practices in a lower risk and more productive way. Nestlé holds 33% of the global market share of coffee and are the single largest player by over 20%.xxiv Therefore, they have the greatest potential to have a positive impact across the coffee supply chain as well as having the most to lose if they do not take action.

2: Cocoa

2.1 The history and geography of cocoa

Cocoa has similar origins to coffee in colonialism and slavery. Cocoa grows on the equator, in the Caribbean and Central America. Currently, the largest volumes of cocoa come from Côte d'Ivoire (40% of global supply) and Ghana (20%), Brazil, and smaller Latam countries are responsible for the remaining 40% of volume.xxv The flavour which the global north associates with cocoa - sweet and fudgy - is the flavour profile of West African cocoa bean equivalents.xxvi While the majority of Latam has volcanic soil and cannot be used to grow cocoa due to the presence of heavy metal. Where it does grow, the flavour profile differs to West African growth.

Climate change is having a significant impact on Cocoa, this has been seen in the extreme price volatility over the past three years. The futures market began rallying in mid-2022 with the price skyrocketing in early 2024 to over 12,000 USD/T. This volatility has shown climate change has a material impact on the profitability of consumer goods companies. If businesses do not improve supply chain resiliency by ensuring fair pay for farmers to implement regenerative agriculture, agroforestry and the prevention of deforestation, then the financial consequences could be significant.

2.2 West Africa

For this piece we will focus on the supply chain within Ghana and Côte d'Ivoire due to the dominance these countries have in the production of cocoa. Like coffee, cocoa has been responsible for a third of the deforestation which has occurred in Côte d'Ivoire and Ghana, both countries have lost 94% and 80% of their forests respectively in the last 60 years. This has had an immediate impact on the cocoa crop as forest provides climate stability, essential shade, flood protection and maintains soil quality.xxvii Unlike coffee, the Ghanaian and Ivorian governments play a key role in global cocoa trade. They control the growing practices and pricing of cocoa in West Africa, as they set the ‘Farmgate’ price. This is a system where the price the farmers will be paid for their cocoa is set ahead of the harvest by the government. The structure was originally designed to protect farmers from the volatility of the trading market, ensuring they were paid a certain amount regardless of market speculation.

The farmgate price is beneficial when the price of cocoa is low, but when the price increases farmers lose out on a monumental scale. When the price increases, farmers under farmgate are then paid much less than the market value of cocoa. In a similar manner to coffee, the value distribution within the cocoa supply chain is structurally unfair. The value of cocoa is realised in the finished, chocolate products which are worth five times more than the unprocessed bean.xxviii West Africa exports nearly all of the cocoa beans it produces and 78% of cocoa grinding is done in developed countriesxxix meaning those countries get the upside of the value of chocolate rather than the growing regions.xxx A solution to redistribute value in the supply chain is to develop processing plants in West Africa. This is what the company Fairafric are doing in Ghana where 60% of the cocoa farmers live below the poverty line. Fairafric believe that by creating better paying jobs in processing cocoa beans, you can create demand for cocoa which in turn supports supply. This moves the industry away from development aid which does not create demand and gives no long-term solution.xxxi

It is estimated that two million cocoa farmers operate three or four hectares of land for cocoa and have an income of less than $1 per day.xxxii The underpayment for the raw commodity of cocoa beans has led to significant levels of child and forced labour in the supply chain. According to the European Bank for Reconstruction and Development (EBRD), over 85% of cocoa is produced in countries where the cocoa sector has been identified as using child labour. Awareness of this issue came to light in the 1990s but very little improvement has been made, with a 14% increase in child labour in Ghana and Côte d'Ivoire between 2008 and 2019. Child labour is hazardous work, involving heavy loads, sharp tools and exposure to dangerous agrochemicals. Child labour has developed because cocoa farmers are not paid enough for their product to pay an adult wage, therefore they employ children at a lower wage or employ their own children for no payment. These children cannot access an education and become stuck in the cycle of poverty. Alongside child labour is forced labour, in West Africa this is generally forced child labour from migrant children. Children are sold to traffickers, kidnapped or migrated willingly but become victims of traffickers. The children will not be able to leave the cocoa farm until their cost of purchase has been worked off, they are often held against their will with no payment for their work.xxxiii

Another key factor to the crumbling reality of cocoa production in West Africa is the nature of the plant itself. Much like coffee, it is a fragile crop that requires an incredibly specific environment. One centigrade or a millimetre of rain can make or break the yield of a cocoa plant. This is why cocoa needs to be grown 20 degrees north and south of the equator.xxxiv Currently there are three major cocoa plants -the Forastero, Trinitario and Criollo. However, the introduction of the ‘Mercedes’ cocoa plant (Theobroma) is disrupting this norm. The Mercedes has a greater immunity to diseases and produces a higher yield than traditional plants. Most importantly, the Mercedes can produce fruit in 18 months,xxxv whereas, traditional cocoa plants take four to six years to bear fruit. The pressure applied to the cocoa plant in recent years has driven research and development into more robust cocoa varieties whilst managing the flavour profile.xxxvi This gives hope to the West African countries, particularly Côte d'Ivoire where Cacao Swollen Shoot Virus (CSSV) is far more established.

Cocoa is a slow crop; in an entire year one plant will produce around 200 grams of processed chocolate. This is two chocolate bars per tree and the older the tree is, the less it will yield. Climate change, deforestation and diseases such as CSSV and Black Pod, exert further pressure on these fragile trees whose yields are already stretched. This is what we have witnessed over the past three years and is the root cause of the extreme cocoa price increase.

CSSV is the most common disease for cocoa trees. It takes hold of the plant via the mealybug in the soil, reducing the yield by 25% in the first year and killing the tree entirely in three to four years. Much like coffee, rain and temperature are the key factors in cocoa’s success. However, the recent inconsistent rain coupled with higher temperatures, has increased the rate of disease as the mealybug thrives in volatile weather. Throughout 2024, over 200 million cocoa trees were impacted by CSSV in Western Africa.xxxvii Matthew Abraham - the Cocoa analyst at Berenberg Research - explains that cocoa farmers are so poor that they have limited resource to defend against the virus due to the price and availability of pesticides and fertilisers.

One solution to these issues could be re-planting cocoa trees under canopy using regenerative agriculture and agroforestry. This would ensure that the supply of cocoa would become more stable in four to six years. However, there is another issue. In 2018, the governments of West Africa prohibited farmers from planting seedling cocoa trees in order to preserve the price of cocoa at the time. However, this legislation is still in place and as the CEO of Barry Callebaut said, ‘we need to continue to get allowance to go for seedling planting again’. He emphasised that the low farmgate price in these countries curtails that incentive for cocoa farmers to increase planting.xxxviii As a result farmers are likely to move away from cocoa to more resilient crops or to go into illegal gold mining which is much more lucrative and is often found in the same land on which cocoa is grown on.xxxix

Cocoa has become a prime example of pushing the environment and the people operating in it too far, with too little resource and unfair value distribution. Fundamentally, cocoa has been too cheap for too long and it has resulted in the price increasing 4,000 USD/T which has had significant financial implications for companies involved in the cocoa supply chain. Cheap chocolate hides the real price paid by the farmers and their environment.xl In order for companies to have a secure supply of cocoa in the future they need to pay their farmers more for the land to be stewarded appropriately, for yields to increase and for productivity to be optimised. None of this can be done if farmers are living in extreme poverty.

2.3 Is luxury the answer?

We have discussed the virulent cocktail of issues facing the cocoa supply chain, but what does this mean for the companies exposed to cocoa within Evenlode’s investment portfolios?

Evenlode is exposed to the cocoa supply chain through investing in Lindt & Sprüngli and Nestlé. Nestlé is held in EGI and Lindt is held in EGE. Nestlé is only exposed through their confectionary channel which makes up 9% of the overall revenue. In addition, the majority of products they sell involve chocolate as an addition to biscuit or cake - such as the KitKat - these products can be marketed without using the word ‘chocolate’ and therefore require a much lower percentage of cocoa solids and butter. For Lindt, 100% of their products are dependent on cocoa and it accounts for 60% of Lindt’s raw materials. They are materially exposed to all the risks we have covered. However, they have the power of premiumisation. Lindt’s products are tablets, boxed assortments or seasonal chocolate. Both Nestlé’s and Lindt’s products will require a certain percentage of cocoa solids and butter depending on the region they are sold. For example, in the EU, Milk chocolate must contain at least 25% total cocoa solids, and dark chocolate must contain at least 35% cocoa solids. In the US however, milk chocolate must contain at least 19% chocolate liquor and dark chocolate must contain at least 35% chocolate liquor.xli

Nestlé has been managing the increased cocoa price by reducing the percentage of cocoa solids and remarketing products such as their white KitKat. They can no longer use the word ‘chocolate’ in the selling of the product because it contains less than 20% of cocoa butter and cocoa solids. Therefore, it is sold as a ‘KitKat 2 finger white biscuit bar’. In addition, Nestlé is insulated against the cocoa price volatility somewhat due to their product offering being much more diverse than that of Lindt.

Lindt however, has been managing the increased cocoa price through premiumisation, increasing their prices by 6.3% through 2024, with the intention to continue increasing prices in the double-digit percentage range during 2025 to offset the high cocoa price.xlii Lindt sell a premium gifting product, this means consumers will take more price inflation without changing their behaviour. Nestlé however, sell everyday products where price inflation will be felt more keenly by the consumer. The high cocoa price is negative for all members of the cocoa supply chain, however Lindt hedges cocoa up to 18 months. This means they have a certain amount of security in their supply chain. In addition, other ingredients such as sugar are deflating in price which support their ability to manage the increased costs within cocoa. When these elements are considered, Lindt is in one of the strongest positions of all cocoa sellers as they can push price due to their lack of exposure to everyday snacking. Nestlé, however, will struggle to do this.

Finally, the European consumer is becoming more elastic and reducing demand for chocolate. Nestlé are more exposed to this than Lindt due to Lindt’s exposure to gifting and special occasion chocolate. Although over the short term both Nestlé and Lindt will be able to manage the increased prices for differing reasons, this does not prevent future risks due to climate change, disease and poor human rights in the supply chain. In order to preserve their supply chain - especially for Lindt - they need to invest in fair distribution of value and sustainable farming solutions for cocoa.

2.3.1 What are Lindt and Nestlé doing about this risk?

Unlike other chocolate companies that rely on external certification such as The Rainforest Alliance, Lindt has their own ‘Lindt & Sprüngli Cocoa Farming Program’. This program was launched in 2008 and aims to ‘contribute to the creation of decent and resilient livelihoods for cocoa farmers and their families and to encourage more sustainable farming practices’.xliii Through this program, they sourced 61.3% of cocoa equivalents (beans, butter and powder) and another 23% of bean equivalents from other responsible sourcing programs in 2024.xliv By the end of 2025 they aim to have responsible sourcing of cocoa equivalents up to 100%.xlv The farming program aims to address all the issues discussed including increased resilience of farming households, reducing the risk of child labour and conserving biodiversity and natural ecosystems. The program is built on four pillars made up of: 1. Traceability of beans; 2. Training farmers; 3. Investment for farmers and the community; 4. Independently verifying their program.xlvi On traceability, they register farmers in order to gather baseline data about the farms which includes the farms GPS coordinates and farm polygons. They then assess the farmers needs and design the program. This allows them to establish a sound traceability system of cocoa beans from the cocoa origins to Lindt. This process is known as ‘bean to bar’.xlvii

The Cocoa Farming Program provides training for farmers on agricultural practices, environmental practices, social practices including child labour and business practices. The third pillar invests in farmers and communities by providing disease resistant cocoa seedlings as well as shade equipment to increase productivity and resilience. They provide cash or in-kind premiums for tools and inputs on top of the market price for cocoa. They also have a child labour monitoring remediation system including investments in education infrastructure. Finally, they independently verify this program by conducting annual internal monitoring of farmers, annual external assessment by a third party and identification and implementation of corrective actions based on the data gathering in order to continuously improve.xlviii

However, although Lindt may be making improvements, they are still lagging best practice. According to The Chocolate Scorecard, Lindt is ‘starting to develop and implement good policies’ and they are particularly strong in deforestation and climate, making significant progress in the last four years.xxvii However, Lindt are a laggard on living income, agroforestry and pesticides. They sit at 13th out of 39 in the global market across the score card. This lower score may reflect the smaller company size of Lindt in comparison to the likes of Mars. However, the highest performers are Tony’s Chocolonely and Ritter Sport, both of which are significantly smaller companies than Lindt with best-in-class policies regarding cocoa sourcing.

Lindt has work to do on achieving their supply chain targets. They have a 15% gap to close in the year of 2025 to reach their 100% sustainability sourced targets which seems unlikely given the last mile is always the hardest. However, given Lindt’s complete dependence on the cocoa crop, they will have to invest in long term supply chain resilience. In addition, the family ownership of Lindt will likely improve the long-term outcome for the business. The bean to bar modelling of their supply chain is essential for this progress to take place and it is encouraging to see the progress Lindt is making.

2.3.2 Nestlé policies

The primary difference between Nestlé and Lindt is that Nestlé does not operate a ‘bean to bar’ supply chain. Nestlé’s suppliers of cocoa are: Cargill, ECOM, ETG/Beyond Beans Foundation, Farmstrong, OFI, Barry Callebaut, GCB, JB Cocoa, OFI, Cocoa Team/So B-Green, Touton and Sucden.xlix They work with these suppliers to implement The Nestlé Cocoa Plan for KitKat and AfterEight along with their Income Accelerator Program. This program is centred around school enrolment, agricultural practices, agroforestry and diversified incomes.

Through the plan they aim to achieve 100% cocoa sourced through the programme and in 2024, 88.94% of cocoa was sourced through the programme.l However, this only applies to two of the Nestlé brands – KitKat and AfterEight.li It does not include Milkybar, Smarties, Aero, Rowntree’s and Quality Street. This is where Nestlé is weaker - they have a strong policy in some areas but misleading marketing around some of their policies. They cannot have 100% sustainable sourcing through the plan when they have over 50% of the land untraceable for deforestation.lii

Nestlé do not have direct oversight of their supply chain but given the proportion of revenue chocolate is accountable for (<8%), this is a sensible sourcing model. Where Nestlé struggle is the traceability of their cocoa supply. Nestlé’s deforestation data for cocoa states that only 46.4% of their primary supply chain is traceable and deforestation-free, this accounts for 335.3 kilotons of cocoa equivalents.liii Therefore, Nestlé need to work with their primary suppliers to develop better traceability throughout their supply chain. This is a significant challenge because of the mass balance sourcing model. Nestlé would benefit from collaborating further by joining programs such as Tony’s Open Chain which exist to end exploitation in cocoa.liv Nestlé do not need to have bean to bar traceability, but they have a long way to go before they can be considered a sustainable seller of cocoa.

To conclude, there has been short term recovery in the cocoa price in recent months, and the price has stabilised around 6,000 USD/T but futures are still 200% higher than three years ago. The crop for 2025/2026 looks to be flat or slightly reduced in comparison to the 2024/2025 crop.lv The recent rebound in port arrivals is reflecting an easing of transportation and financing constraints rather than a surge in production. Continued tightness in supply with variable weather and logistical challenges will be the reality of the short-term cocoa outlook.lvi If changes are not made by companies, this short-term outlook is likely to become the permanent long-term outlook. Nicolas Mounard, the VP of ESG, Sustainability & Traceability at Barry Callebaut states that ‘insights point to a substantial gap between current investment levels and what is truly needed to drive lasting change’.lvii This highlights the unfair distribution of value throughout the supply change and the importance of changing the status quo of both coffee and cocoa from being broadly unsustainable products with some exceptions such as Tony’s Chocolonely and specialty coffee, to all products being sustainable as the baseline. In order to perform this paradigm shift the investment needs to go to on-farm improvements, protecting forests and ensuring equitable value distribution.

3: Conclusion

The coffee and cocoa industries have structural issues stemming from colonial origins and subsequent commoditisation. The relentless exploitation of people and the environment have resulted in persistent social injustices, such as forced and child labour, and severe environmental degradation, such as deforestation, biodiversity loss and declining soil quality. Hundreds of years of unsustainable practices have led to price volatility and are now jeopardising the long-term viability of these crops, and the people and companies that are reliant upon them.

Lindt and Nestlé are exposed to the risks of the coffee and cocoa supply chains. They are now facing the consequences of underinvestment in sustainability and fair value distribution through the supply chain. To secure the future of coffee and cocoa, and to ensure the long-term resilience of their supply chains, both companies must embrace the paradigm shift. They must redistribute the value of their supply chain by paying farmers the fair price, investing in regenerative agriculture at scale, and adopting fully transparent and traceable sourcing practices.

These changes will require short-term margin pain in order to maintain long-term top line growth and prevent the eventual collapse of supply. Shareholders and investors have a critical role to pay by pushing for these improved sustainable practices and accepting the necessary short-term margin pain for the long-term gain. Without a more equitable and sustainable approach, coffee and cocoa yield will continue to suffer and prices will remain unsustainable. Therefore, only through meaningful change and investments can these commodities thrive in the decades to come.

Important information

Evenlode has developed a Glossary to assist investors to better understand commonly used terms.

This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject to change and are not guaranteed.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited (IFSL) is authorised and regulated by the Financial Conduct Authority, No. 464193.

Footnotes

-

TNL, ‘Article 52: Coffee Trade Established the Position of the Dutch Power’, Trung Nguyên Legend, 13 October 2020.

-

Livia Gershon, ‘How Coffee Went from a Mystical Sacrament to an Everyday Drink’, JSTOR Daily, 8 October 2017.

-

'Coffee's Destruction of Brazilian Forests and its Future'. Coffee Watch. October 2025.

-

‘Riskmap.Fairtrade.Net/Commodities/Coffee’, n.d.

-

Ibid.

-

'Coffee's Destruction of Brazilian Forests and its Future'. Coffee Watch. October 2025.

-

Ibid.

-

‘About 97% of the Atlantic Forest Consists of Parts Smaller than 50 Hectares | WWF Brazil’, 27 May 2024.

-

‘The Brazilian Coffee Cycle: From Flowering to Harvesting’, Atlantica Coffee, 29 November 2023.

-

What Do Chinese Coffee Buyers and Consumers Want? - Coffee Intelligence, Production & Trade, 4 November 2025.

-

‘Coffee's Destruction of Brazilian Forests and its Future'. Coffee Watch. October 2025.

-

‘Statistics - Euromonitor: Passport’, n.d.

-

A non-profit watchdog organisation.

-

‘What Is Agroforestry?| Soil Association’, n.d.

-

Coffee's Destruction of Brazilian Forests and its Future'. Coffee Watch. October 2025.

-

‘Riskmap.Fairtrade.Net/Commodities/Coffee’, n.d.

-

Statistics - Euromonitor: Passport.

-

Ibid.

-

‘Insights | Lombard Odier’, 8 September 2025.

-

Cocoa bean equivalents refer to the sum of all cocoa products such as cocoa butter, cocoa power etc. converted into cocoa beans by the conversion factors set by the International Cocoa Organisation (ICCO).

-

‘Chocolate Scorecard’.

-

‘Insights | Lombard Odier’.

-

‘Cocoa Facts and Figures - Kakaoplattform’, n.d.

-

‘Insights | Lombard Odier’.

-

Ibid.

-

Damien Gayle, ‘Cocoa Planting Is Destroying Protected Forests in West Africa, Study Finds’, Environment, The Guardian, 22 May 2023.

-

‘Cocoa’, Verité, n.d.

-

‘Cocoa Growing’, Cocoa Life, n.d.

-

CocoTerra, How Long Does It Take to Grow a Cacao Tree? | CocoTerra Company, 19 February 2023.

-

‘Chocolate and Coffee: Similarities and Differences between Cocoa and coffee beans’. theyo.25 January 2023.

-

CocoTerra, The Latest Cacao Virus: CSSV Threatens Global Chocolate Production, 6 June 2024.

-

Barry Callebaut negotiates with Ivory Coast and Ghana to change Replanting Laws, reports flat sales volume. Food Business Middle East & Africa, 8 November 2024.

-

Dr Kirsty Leissel - Bernstein Webinar: A discussion of the cocoa outlook with Dr. Kristy Leissle, CEO of African Cocoa Marketplace.

-

‘Tony’s Chocolonely Boss Says Investing in Farmers Is Good for Business’. Financial Times. 14 September 2025.

-

‘What Is the Legal Definition of Chocolate?’, CocoaSupply, n.d.

-

Anthony Myers, ‘Lindt Warns of Price Increases, Sees Rise in Responsible Cocoa Sourcing’, From The Desk of CocoaRadarTM, 5 March 2025.

-

‘Home - Farming Program (by Lindt & Sprüngli)’, n.d.

-

‘Lindt & Sprüngli Sustainability Report 2024’, n.d.

-

Ibid.

-

‘Lindt Sustainability | Intl’, n.d.

-

‘Bean to Bar - Farming Program (by Lindt & Sprüngli)’, n.d.

-

‘About the Farming Program - Farming Program (by Lindt & Sprüngli)’, n.d.

-

‘Income Accelerator Program Report Progress Report - June 2025.Pdf’

-

‘Sustainable Cocoa | Cocoa Cultivation | Nestlé Cocoa Plan’, n.d.

-

‘Nestlé’s Sustainable Cocoa Brands | Nestlé Cocoa Plan’, n.d.

-

‘Deforestation-Free Supply Chains | Nestlé Global’, n.d.

-

Ibid.

-

‘Tony’s Open Chain Exists to End Exploitation in Cocoa, Together’, n.d.

-

Matthew Abraham, Cocoa Climate Monthly: October 2025.

-

Ibid.

-

Anthony Myers, ‘Barry Callebaut Puts a Price Tag on Cocoa Sustainability’, From The Desk of CocoaRadarTM, 14 November 2025.