As selectors of companies on our clients’ behalf we are keen to report on how the ones in the portfolios we manage are performing on the ground. Our colleagues on the IFSL Evenlode Income and IFSL Evenlode Global Equity strategies have done just that recently, as indeed we did from a Global Income perspective a month agoi. We have also been keen to note just what good value those companies seem to be trading at in the market, a situation that has not changed materially over recent weeks. We haven’t been alone in observing that many high-quality businesses have been underperforming in the market, leading to those compelling valuations. Various articles, comments and analyses suggest similar, often looking at an off-the-shelf index that categorises companies on the basis of their financial characteristics versus a broad market indexii.

Articles stating that ‘quality has underperformed’ certainly ring true with our lived experience as investors that look for market leading companies with solid financials and dividend-growing capabilities. Thinking about where the action has been in the market it kind of makes sense. Banks and Capital Goods companies that have historically generated low returns on capital have been on the up, as well as unprofitable technology companies.

But it only kind of makes sense because whilst directionally we might expect solid businesses to underperform in a robust economy, the magnitude of the differential for certain businesses has been dramatic. The global economy is patchy rather than robust. Also, broad-brush statements about quality’s performance depend on what index is examined, and over what time period. Bringing in questions of valuation make the whole picture a bit perplexing, as we’ll touch on below.

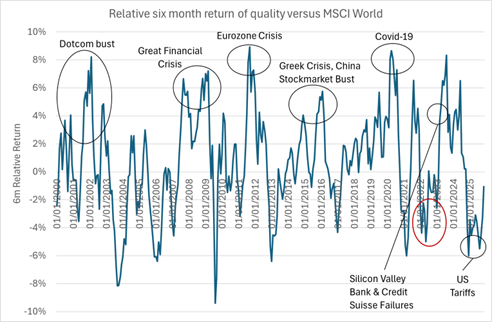

Taking the MSCI World Index as a guide illustrates some of the challenges in the narrative around quality. The chart below shows the six-month relative return of the ‘quality’ sub index, compared to the headline MSCI World Index. Whilst it’s as noisy as any other time series in financial markets, it does seem that on the whole quality’s outperformance since the turn of the Millennium has come in times of economic or market stress.

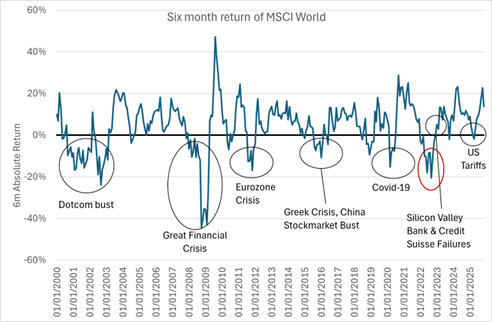

Casting the same episodes in financial history on a chart of the rolling six-month absolute return of the MSCI World Index confirms that the outperformance of quality is indeed generally when equity markets are more challenged.

But more recently something different appears to be happening. The time circled in red on both charts represents a sell-off, particularly in Information Technology companies, in 2022. There were concerns at that time around rising inflation and interest rates, but also about valuations that had expanded through the coronavirus pandemic. Once that had bottomed and the mini financial crisis of spring 2023 had been stabilised, there has not been much market stress despite the occasional headline. Even the tariff-related volatility barely features as a negative on the chart above in historical terms. It was, though, a recent low, and in that brief period quality underperformed, bucking the defensive characteristics previously shown. The sub-index’s relative performance has recovered in the market rebound.

Quality also underperformed in the 2022 sell-off. It doesn’t take too much analysis to figure out that the quality index has become dominated by the same technology companies that dominate the broader market. The market action would suggest so, and a quick use of your favourite search engine (no AI required) finds the Magnificent 7iii atop quality indices. This, then, brings us to the much-discussed question of valuation.

One would normally expect to pay up for quality, and indeed this is the case at the current time. At the time of writing the price/earnings multipleiv on the MSCI World Index is about three ‘turns’ below that of its quality sub-index. Going back ten years, that figure was two turns, so quality has got a bit more expensive relatively speaking. But the absolute figures are important, or at least they should be. Ten years ago the MSCI World Index traded at a multiple of 18x, now it is 24x. The gap between quality and the rest is in fact higher, because the ‘quality’ sub-index included in the broad index.

To say it again, we have been very keen in recent times to note how the Evenlode portfolios look to be trading at unusually attractive valuations, which runs counter to the quality narrative above. We are able to achieve this because we don’t, of course, invest in indices. We invest our clients’ capital in companies, and we can select ones that meet our quality criteria but also trade at sensible valuations. The businesses in the IFSL Evenlode Global Income portfolio are trading at a multiple of 18x as a weighted average, a figure that has a distinctly 2015 air about it. In fact, better than 2015, because 18x would have been in line with the broad index back then, and our collection of companies exhibits quality characteristics across many financial and qualitative dimensions.

The makeup of an index or fund thus matters, and matters even more if valuation is taken into consideration, as we believe it should do as active investors looking to manage and balance long term risk and return. Further, indices that have different entrance criteria can prove to switch behaviour between different market regimes.

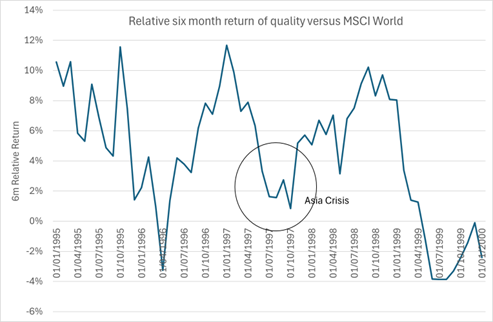

The previous charts start at the turn of the millennium. That’s not just a memorable moment in time because 2000 is a round number, it’s also a memorable time in stock market history. The crescendo of the dotcom boom was just about to turn the other way, and the quality index was hitting its stride in relative terms. Rewind the clock a little further and we see that quality did pretty well prior to the bursting of the bubble, but interestingly less well in a relative sense when there was an economic wobble in the form of the Asia Crisis. That was another time when markets were roaring, valuations were high, and perhaps some of the usual relationships between indices with differing characteristics broke down.

Quality as an idea has shown itself to be valuable over long periods of time. In these periodically strange sorts of markets, as we are undoubtedly in now, we think it is particularly important to look beyond the style and focus on its application to individual companies. We hope you forgive the diversion to discuss market indices, but we think it serves to highlight the challenges of piecing together market narratives and indeed choosing benchmarks.

Neat narratives ignore the messy reality of markets where differing actors bid prices up and down for variant reasons, and correlations that seem plausible and even explanatory can change or break down through time.

Our focus is on identifying great businesses and assessing their valuations, and whilst not easy, is at least a simpler proposition. The changes in market regime can create opportunities. At the moment at the granular stock level the market is, despite the expensive level of both the broad and ‘quality’ indices, throwing up some interesting propositions that may find their way into the portfolio.

Ben Peters and Rob Strachan

28 November 2025

Evenlode has developed a Glossary to assist investors to better understand commonly used terms. This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject t0 change and are not guaranteed.

IFSL Evenlode Global Income is a sub-fund of the IFSL Evenlode Investment Funds ICVC. Full details of the Evenlode Funds, including risk warnings, are published in the IFSL Evenlode Investment Funds Prospectus and the IFSL Evenlode Investment Funds Key Investor Information Documents (KIIDs) which are available on request and at www.evenlodeinvestment.com.

The IFSL Evenlode Investment Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, IFSL Evenlode Global Income may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future. Market data is sourced from S&P Capital IQ, Financial Express Analytics and Bloomberg unless otherwise stated.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com).

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.

Spring Capital Partners Limited is an Appointed Representative of Robert Quinn Advisory LLP, which is authorised and regulated by the Financial Conduct Authority, with FRN 548030.

Footnotes

-

Here is one example from the FT: https://on.ft.com/4nDYUIg

-

The Magnificent Seven refers to seven dominant US tech companies—Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla—that played a crucial role in driving market growth over recent years.

-

Price/ earnings multiple - A measure of a company’s current market valuation compared to its earning potential, calculated by dividing a company’s share price by its Earnings per share (EPS).