The portfolio ended the year with a net asset value (NAV) per share almost exactly where it was on 31 December 2024 in GBP terms, albeit it was up 7% in USD terms. This is a very disappointing result given the 21% increase (USD terms) in the MSCI World Index, our comparator benchmark, and we are dissatisfied with where we are. But rather than despairing, we think this is an exceptionally promising period for investment. We have spent the past year closely checking company health metrics and these continue to be good; we trust investors will excuse us for continuing to refer to them, on the analogy that a map needs more frequent checking in foggy weather.

Active equity management depends on market valuations being more volatile than company fundamentals. In a rational world the price of companies would track their long-term cashflow outlook, but this would leave little or no gain to be had in investing away from the market core. Shares are unusual assets; people want them less when prices are lowi. We would prefer that the dislocations be smaller than the one we experienced in 2024-2025, but we also recognise that the launch of AI technology is a once-in-a-generation event. Evenlode has always focused on controlling the controllables, by designing a business and an investment process that accommodates the natural volatility of equity markets, while attracting like-minded investor base which understands the unevenness of equity returns.

It is unequivocally negative that NAV per share of the fund has lagged the comparator benchmark over the last year. It is positive, on the other hand, that on our calculations the underlying portfolio company revenues have increased by +8%, adjusted operating profit by +12.7%, and Earnings per Share (EPS)ii by +23% over the last 12 months (as companies have not yet reported their results for the quarter ended 31 December 2025, we are referring to the period 1 October 2024 to 1 October 2025; Quoted figures are averages based on portfolio weightings). This is comfortably greater growth than the MSCI World Index which, on Barclays estimates, produced +4% revenue growth and +8% EPS growth in the same period. Free cash flowiii growth has also been solid and increasingly superior to the index, where the growing bill for AI capital investment is beginning to stress the balance sheets of the largest index constituents.

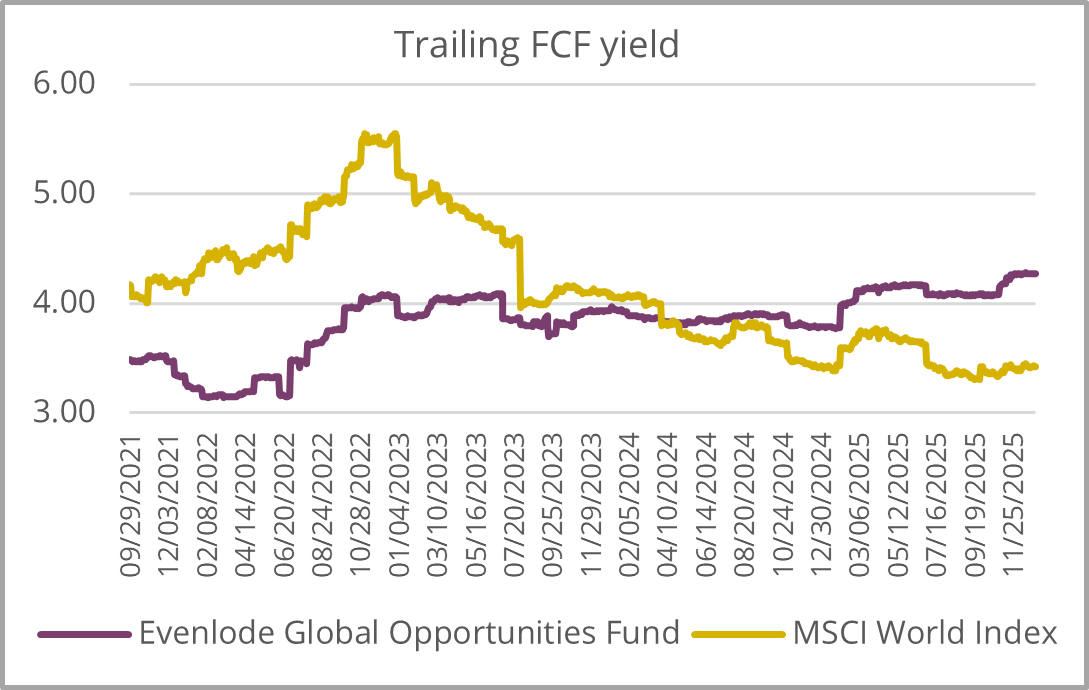

This combination of superior fundamental growth, flat share prices, and a +21% increase in the benchmark index means that the portfolio is now dramatically cheap compared to the broader index on the simple metric of price to free cash flow.

Source: Bloomberg.iv

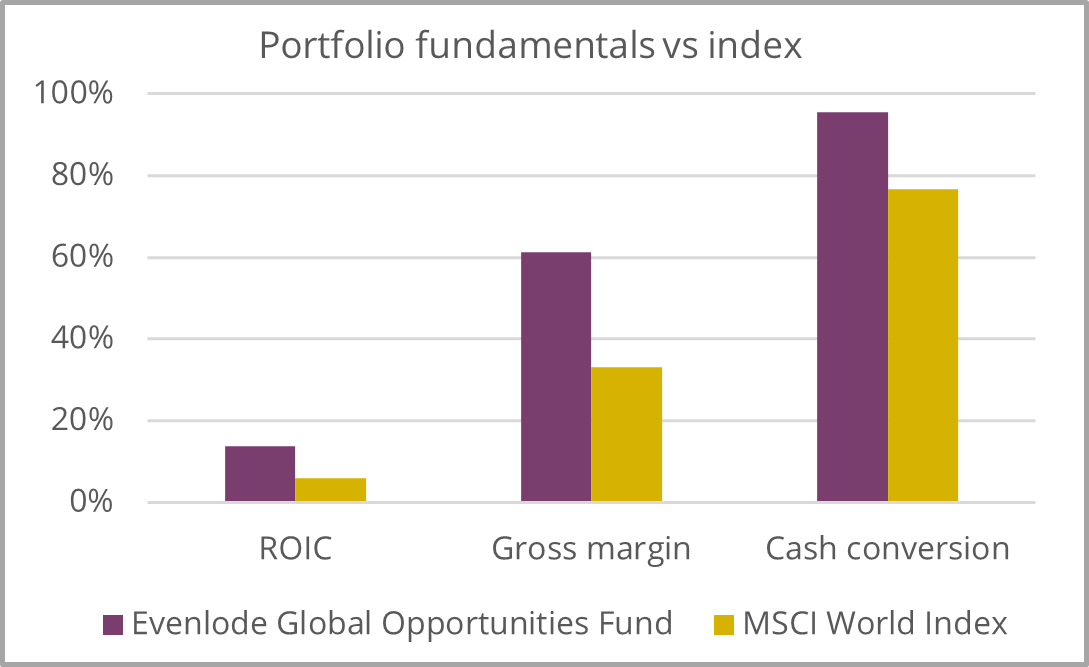

This discount widens if you want to give the portfolio credit for its superior financial characteristics, as below. Evenlode’s investment process is built on the thesis that fundamentals cannot remain divorced from prices indefinitely, and the longer the period of underperformance the bigger the ‘giveback’ will be when prices start to reflect these fundamentals.

Source: Bloomberg, Evenlode.v

Recent disappointing fund performance, then, only makes sense if we assume that the near future will bring an abrupt end to this steady progression in portfolio revenues and profits. Thankfully, we believe this scenario is overwhelmingly unlikely.

Our relative performance problems in 2025 had two origins, both related to AI. Firstly, our focus on enduring earnings power with low cyclicality and higher diversification kept us away from the biggest drivers of index returns which skewed towards cyclicalvi and capital-intensive companies – banks, semiconductors, and other capital goods manufacturers. Secondly, our preference for these qualities meant we had high weights in industries which are being bucketed by the market as ‘AI losers’ like information services. Extensive due diligence in the year both by us and other investors and analysts has demonstrated that the AI threat to existing data assets is largely a phantom menace. A probabilistic approximate retrieval system which is inherently unstable iteration to iteration is perfect for drafting marketing emails and okay at summarising conference calls, but a literal liability in sensitive, highly regulated deployments like credit and insurance underwriting and legal citation retrieval. As long as the state-of-the-art AI architecture is the large language model (LLM), this is likely to persist. We are in a strange moment in that the AI disruption thesis is widely discounted, but investors remain reluctant to buy companies in the ‘penalty box’ for reasons of career risk rather than on fundamental objections.

We need to stress that we are not negative on AI as a technology; it has considerable potential in many areas, although we believe it has been oversold as a universal panacea. Numerous companies we are invested in will benefit if AI can show more general returns on investment. Some are already clearly benefiting, most spectacularly Alphabet which has generated attractive returns from incorporating machine learning models into Search and other properties. If the resolution to the trade is widespread demonstration of returns on AI investment, we think this is paradoxically great for the wider stock market and less great for the AI complex of semiconductors and capital goods companies. The stock prices of these companies are already pricing in a ‘forever bull market’ in data centre construction, but the rest of the market is pricing in little to no returns from this construction. We expect this dissonance to resolve itself one way or the other, and the rapidly increasing weight of bets on outcomes, and the increasingly high cost of placing these bets consequent to leverage, continually shortens the time the bets can be left open.

There is now widespread recognition that AI is very unlikely to revolutionise the worlds of enterprise data and software. Three years of determined effort and lavish spending have produced dismayingly modest results outside of software coding. The market conversation on AI has moved on from discussions of what it could achieve to trying to identify which year of the late 1990s we are in in terms of the stock market cycle. If we are in 1996 or 1997, the logic runs, there is every reason to stay invested for one more year before bailing out. For us, this liquidity-driven rather than solvency-driven approach to investing means that the underlying assets are irrelevant to the decision so long as their owner is confident an even more enthusiastic buyer will be around for them in the future. In a market which has deprioritised fundamentals, securities are more likely to trade at prices which are disconnected from their economic future, and investors have good opportunities to bake in very attractive future returns.

This takes us to a common and sensible point investors have made to us – when do things change? It is much easier to be confident about the next five years than the next five months. Timing market rotations is notoriously one of the hardest things to do in financial markets, far harder in our experience than identifying resilient business models. That said, the AI trade is materially different as we start 2026 to what it was way back when it kicked off in 2023. Firstly, the numbers are vastly bigger. The key AI infrastructure clients had $167bn in capex in 2023 but are expected by sellside analysts to spend $623bn in 2026 (buyside expectations are certainly higher)vii. Secondly, as the likelihood of profitable business models built on current AI recedes, the necessity of more punitively expensive model training to secure a breakthrough just grows and grows, the opposite of the usual dynamic where efficient scaling makes innovation progressively self-funding. Thirdly, the sources of money have shifted. The oft-repeated point that hyperscaler cashflow was funding the trade was completely true in 2023, but this is increasingly not the case, as the size of the tickets being written necessitated a shift to equity and debt markets to fund them. Both increases and decreases in valuations can amplify themselves meaning the trade is intrinsically more fragile and volatile.

The portfolio enters 2026 in great shape. There are pockets of cyclical weakness particularly in the consumer sector where the K-shaped economy is weighing on almost all companies, but in aggregate revenue, profit, and cashflow growth are all solid, leverage is modest, and margins are gently expanding while reinvestment in competitive advantage continues to expand. While earnings delivery keeps up, further derating gets progressively harder. In particular, the opportunity for these companies to exploit their modest leverage and underpriced shares by repurchasing their own stock is getting more and more compelling.

We acknowledge that the last year and a half has been disappointing, and we thank our investors for their patience and understanding. We remain confident that the path ahead for our portfolio companies is extremely attractive, and that there is a silver lining to the rough patch of the last year and a half in the form of a rare opportunity to buy superior companies at a wide discount to the broader equity index.

Chris E, James, Cristina, Gurinder, and the Evenlode Team

7 January 2026

Evenlode has developed a Glossary to assist investors to better understand commonly used terms. This document is not intended as a recommendation to invest in any particular asset class, security, or strategy. The information provided is for information purposes only and should not be relied upon as a recommendation to buy or sell securities. Prospective investors should seek independent financial advice.

This document has been produced by Evenlode Investment Management Limited (‘Evenlode’). Every effort is taken to ensure the accuracy of the data used in this document, but no warranties are given.

Investment commentary represents the opinions of the Evenlode team at the time of writing and does not constitute investment advice. Where opinions are expressed, they are based on current market conditions, may differ from those of other investment professionals and are subject to change without notice. Any forecasts provided are subject t0 change and are not guaranteed.

Evenlode Global Opportunities is a sub-fund of the Evenlode ICAV. Full details of the Evenlode Funds, including risk warnings, are published in the Evenlode Investment Funds Prospectus and the Evenlode Investment Funds Key Information Documents (KIDs) which are available on request and at www.evenlodeinvestment.com.

The Evenlode Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. You should therefore regard your investment as long term. As a focused portfolio of between 30 and 50 investments, Evenlode Global Opportunities may carry more risk than a fund spread over a larger number of stocks. The funds have the ability to invest in derivatives for the purposes of efficient portfolio management (techniques used by investment managers to manage a portfolio in a way that aims to improve returns, reduce risk, or manage costs, without significantly changing the overall investment strategy or risk profile), which may restrict gains in a rising market. Investments in overseas equities may be affected by changes in exchange rates, which could cause the value of your investment to increase or diminish.

Past financial performance is not a reliable indicator of future results. Fund performance figures are shown inclusive of any reinvested income and net of ongoing charges and portfolio transaction costs unless otherwise stated. The figures do not reflect any entry charge paid by individual investors. Tax treatment depends on individual circumstances and may change in the future. Market data is sourced from S&P Capital IQ, Financial Express Analytics and Bloomberg unless otherwise stated.

Evenlode believes that delivering real, durable returns over the long term can be best achieved by integrating environmental, social and governance (ESG) factors into the risk management framework as this ensures that all long-term risks are monitored and managed on an ongoing basis. In addition to reviewing ESG factors when making investment decisions, Evenlode engages with portfolio companies on a range of ESG issues (for example greenhouse gas emission reduction). However, please note that the fund does not have a sustainability objective.

This document is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The sale of shares of the fund may be restricted in certain jurisdictions. In particular shares may not be offered or sold, directly or indirectly in the United States or to U.S. Persons, as is more fully described in the Fund's Prospectus.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com).

EAA Fund Global Large-Cap Growth Equity Sector – © Morningstar 2025. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction.

Evenlode is a trading brand of Evenlode Investment Management Limited. Authorised and regulated by the Financial Conduct Authority, No. 767844. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.

Spring Capital Partners Limited is an Appointed Representative of Robert Quinn Advisory LLP, which is authorised and regulated by the Financial Conduct Authority, with FRN 548030. Spring Capital Partners GmbH and Spring Capital Partners AB are tied agents within the meaning of Article 29 (3) of Directive 2014/65/EU (“MiFID II” as implemented in the respective national legislation) of Allington Investment Advisors GmbH, Kaiser-Friedrich-Promenade 127, 61348 Bad Homburg v.d.H., Germany, which is authorised and regulated by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) with BaFin-ID: 10158575.

The Tied Agents are entered in the public register of tied agents held by BaFin. Within the scope of providing financial services (“investment brokerage” within the meaning of Annex I A (1) MiFID II as implemented in the respective national legislation by promotion of the potential investor's willingness to enter into a transaction but excluding the reception and transmission of orders in relation to one or more financial instruments), the Tied Agents act exclusively on behalf and for the account of Allington Investment Advisors GmbH and undertake to exclusively distribute funds. The information provided by the Tied Agents is intended for informational purposes only and does not represent an offer to purchase or sell financial instruments. All information is provided without any guarantee. This information neither represents any investment / legal / tax advice, nor any recommendation. The Tied Agents point out that every investment decision should be made after consulting an advisor. The information is intended exclusively for professional clients within the meaning of Annex II MiFID II. The information provided may not be copied or further distributed to third parties without the prior consent of Allington Investment Advisors GmbH. The information may not be given to persons or companies that do not have their ordinary residence or domicile in the countries in which Allington Investment Advisors GmbH is authorised to provide financial services. In particular, the information may not be made available to US citizens or persons residing in the USA.

The Fund has appointed as Swiss Representative Waystone Fund Services SA, Av. Villamont 17, 1005 Lausanne, Switzerland, Tel: +41 21 311 17 77, email: Switzerland@ waystone.com. The Fund’s Swiss paying agent is Banque Cantonale de Genève. The Prospectus, the Key Investor Information Documents, the Instrument of Incorporation as well as the annual and semi-annual reports may be obtained free of charge from the Swiss Representative in Lausanne. In respect of the Shares distributed in or from Switzerland, the place of performance and jurisdiction is at the registered office of the Swiss Representative. The issue and redemption prices are published at each issue and redemption on www.fundinfo.com. Evenlode Investment Management Limited is authorised and regulated by the Financial Conduct Authority, No. 767844. The Evenlode Global Opportunities Fund is authorised and regulated in the Republic of Ireland by the Central Bank of Ireland.

Footnotes

-

Reverential quotations of Warren Buffett are an ancient staple of investor newsletters, and in honour of his retirement this one is fitting: ‘We are going to be buyers of things over time. And if you’re going to be buyers of groceries over time, you like grocery prices to go down. If you’re going to be buying cars over time, you like car prices to go down. We buy businesses. We buy pieces of businesses: stocks. And we’re going to be much better off if we can buy those things at an attractive price.’ (From the 1994 Berkshire Hathaway AGM).

-

EPS (Earnings per share): A measure of company profitability, calculated by dividing a company’s profit by the number of shares in issue.

-

Free cashflow (FCF): A measure of how much cash a company can generate over and above normal operating expenses and capital expenditure. The more FCF a company has, the more it can allocate to dividend payments and growth opportunities.

-

FCF Yield: Free Cash Flow (FCF) per share divided by the current share price. A higher Free Cash Flow Yield implies a company is generating more cash relative to its price that could be paid out as dividends and to reinvest into growth of the business.

-

ROIC (Return on Invested Capital): Calculated as net operating profit divided by invested capital. A measure of how effectively a company uses the money it has invested to generate profits.

Gross margin: How much money a company keeps from its sales after paying for the direct costs of making its products or delivering its services.

Cash conversion %: Free cashflow as a percentage of earnings – a measure of how efficiently a company turns accounting profits into cashflow.

-

A cyclical industry is a type of industry that is sensitive to the business cycle, such that revenues generally are higher in periods of economic prosperity and expansion and are lower in periods of economic downturn and contraction.

-

Source - Visible Alpha. This is a limited pool of companies and will include non-AI capex, but also excludes substantial AI capex from companies outside this group and private companies.