Outlook 2017

The philosopher emperor Marcus Aurelius described the art of living as more like wrestling than dancing, a sentiment that could also be applied to navigating investment markets during 2016. A touch of Roman stoicism was required as investment trends changed sharply from month-to-month, with political uncertainty creating meaningful event risk. Viewed over the full year however, it was a positive period for UK investors, with the overall market posting a total return of +16.8%*, helped in part by the falling pound.

Review of 2016

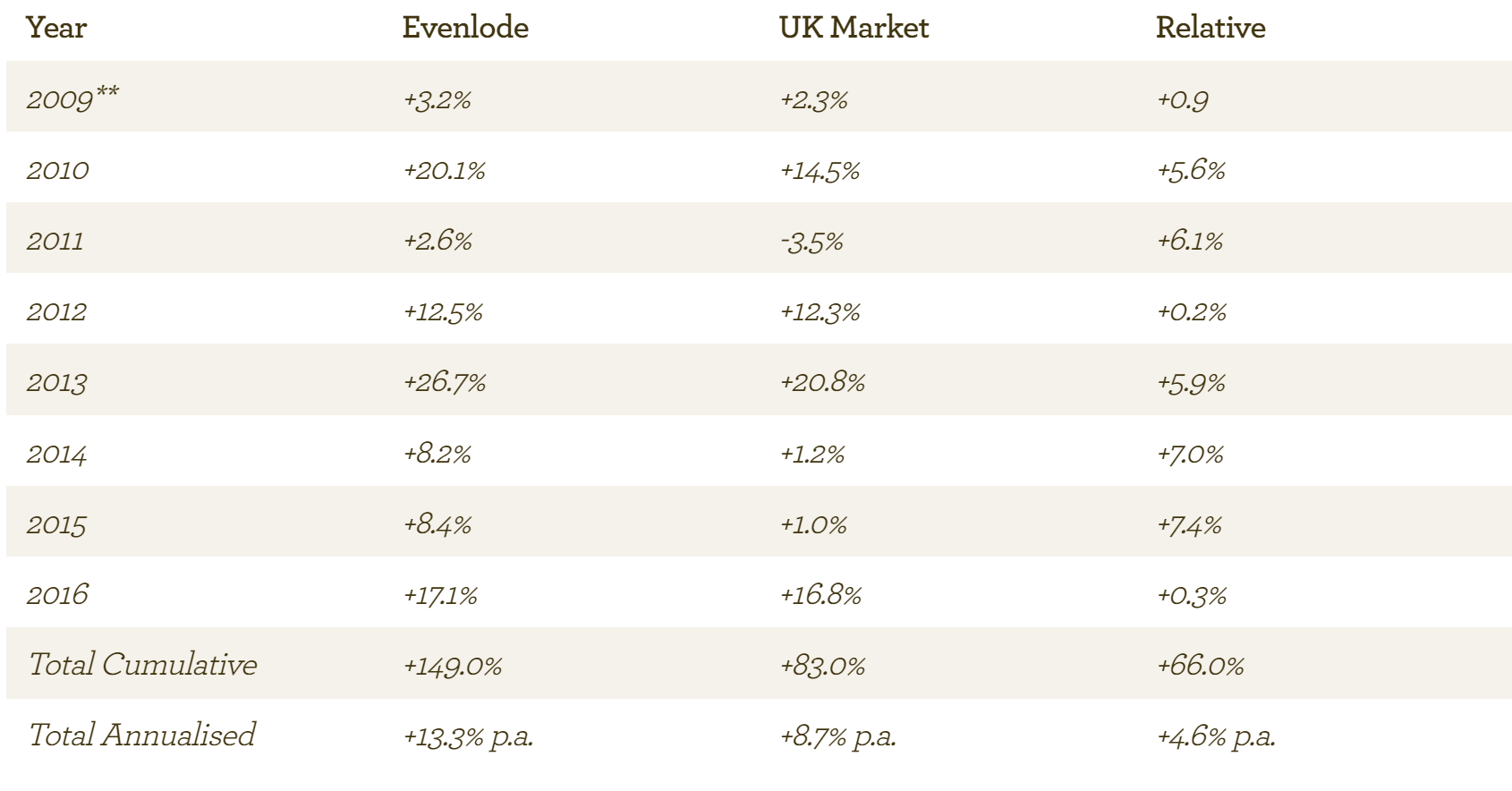

Evenlode rose by a similar amount (+17.1% over the year) though, as with the market, this gain by no means accumulated in a ruler-straight line.

The fund’s focus on asset-light companies leads to a structural lack of exposure to both energy and mining producers. A strong performance from these sectors in 2016 therefore created a significant headwind to Evenlode’s relative performance, particularly in November and December following the US election (the total drag on relative performance from sector allocation was -7.9% over the year, which was entirely due to this zero weighting in resource producers).

Offsetting this trend was good, broad-based performance from individual holdings in the fund, with 37 of the 42 positions held during the year posting a positive return. In particular, it was pleasing to see several newer holdings contribute strongly. Examples included RWS Holdings (+70%), Smiths Group (+56%), Page Group (+39%), Rotork (+36%), Spectris (+32%), Victrex (+29%), Burberry (+29%) and Aveva (+25%). These are all high quality companies that have faced tough end markets over the last couple of years, but continue to generate strong cash flow and invest meaningfully in long-term growth.

The other major theme (for both the fund and the broader UK market) was the pound’s weakness. The share prices of many UK companies with overseas earnings benefited, including key holdings such as Unilever (+16%), Diageo (+17%) and Glaxosmithkline (+22%). US listed holdings in Johnson and Johnson, Microsoft and Procter and Gamble were also helpful to performance.

There were two main negative contributors during the year, IG Group and Mitie. IG Group (-36%) was impacted by an FCA announcement that marked a significant change in attitude towards UK spread-betting regulations. IG has been a long-term holding in the fund and its cash generative business model has produced good dividend and capital growth over the years. However, we decided to exit Evenlode’s position given the risk these regulatory headwinds present over the medium-term. Mitie (-25%) underperformed as customers reduced discretionary spending following the UK referendum. We have reduced the fund’s holding in Mitie on balance sheet considerations, but have retained a 1% position. We welcome the recent change in management and with it a new, simplified strategy: to invest in long-term organic growth (particularly in technology), to focus on cash generation and to dispose of non-core businesses.With another year added to the fund’s life, below are the total returns generated by calendar year

since launch, versus the UK Market*:

Dividends

The dividend outlook for the UK is quite mixed. Dividend cover for the overall market has fallen over the last few years with corporate growth under pressure from a patchy economic backdrop. Debt levels have also been rising, as companies have used low borrowing costs to help fund acquisitions and share buy-backs. Offsetting these factors last year was the significant depreciation in sterling which is helpful for UK companies that earn and/or pay their dividends in foreign currencies. This led to a modest increase in market dividends last year, but without this currency benefit dividends would have fallen. As it stands, 2017 is likely to be a similar year with a difficult dividend backdrop being offset somewhat by the continuing flow-through of currency tailwinds.

In terms of the Evenlode fund, the first three interim dividends for the year ending February 2017 have been increased by +3.6%*** and we expect a similar growth rate for the full year. More generally, our focus on providing real dividend growth over the medium and long-term remains central to our approach. I continue to feel that mid single-digit dividend growth is probably as much as can be expected in the current environment, even from the cash generative businesses we focus on. A higher growth rate is unlikely unless the global economy and/or inflation were to pick up materially.

Outlook 2017

Looking ahead to 2017 plenty of uncertainties await, not least on the political front: Donald Trump is now US president, there will be several important European elections and Brexit negotiations will continue. As I discussed last month, the market has begun to anticipate a pick-up in global economic growth and inflation in recent months. However, structural deflationary pressures remain significant and should not be ignored. In particular, even a small rise in interest rates could cause problems for economic progression given the high stock of global debt.

Turning to valuations, our view has changed little over the last three years or so. Prospects for future returns appear less attractive than they did several years ago (and many stocks that are ostensibly ‘cheap’ on a price/earnings basis carry significant fundamental risk such as high levels of debt and a lack of cash generation). Valuation management remains a key part of our process, and we continue to nudge the portfolio gently towards those areas of the fund and investable universe where we see the most attractive combination of quality and long-term valuation appeal.

More generally, our aim remains to insulate investors from a wide range of political and economic outcomes rather than make big predictions. On this note our focus as we head into 2017 will as usual be on asset-light companies with sustainable competitive advantages. Another characteristic we have been particularly focused on over the last three years is balance sheet strength, given an overall environment in which many companies have been taking on more debt (making them more vulnerable to negative economic developments and/or interest rate rises). The chart below highlights the market’s weakening balance sheet over recent years and our efforts to deliberately move the Evenlode portfolio in the opposite direction****:

Finally, I’d like to mention the development of the Evenlode team over the last few years. The team now totals eight (including an investment team of four) and it is a pleasure working with this talented and dedicated group of people. We look forward to updating you on Evenlode’s progress during 2017 and as always, please do get in touch if you have any queries.

Hugh Yarrow , Fund Manager

19 January 2017

Please note, these views represent the personal opinions of Hugh Yarrow as at 19 January 2017 and do not constitute investment advice.

*Source: Financial Express, total return, Evenlode = B Income bid-to-bid, UK market = FTSE Allshare.

**2009 from launch date (19 October 2009).

***B Inc shares, pence per unit.

****Source: Evenlode, FactSet.